WE’RE FOUR DAYS AWAY FROM MY FIRST “UNOFFICIAL” PERISCOPE VIRTUAL MEET AND GREET!!! It’s going down this Saturday November 21st from 1-2pm CST. I’ll introduce myself, tell you a little bit about me, why I have chosen my current path/what I wish to accomplish, then wrap up with a brief Q&A. Follow The Financial Hack @IAmCoachAndrea for the live broadcast as well as future live broadcasts regarding budgeting, creative saving, financial fitness, personal finance training, motivation and more.

All posts by thefinancialhack

PERISCOPE UNOFFICIAL COMING SATURDAY NOVEMBER 21st!!!

TheFinancialHack.Com Presents…. PERISCOPE UNOFFICIAL!!! Join me SATURDAY, NOVEMBER 21st FROM 1-2PM CST for a Live Q&A Session/Virtual Meet and Greet. You can ask me whatever questions (appropriate, of course) you like, be it questions from my prior YouTube vlogging days to the shift in my priorities and everything else in between. You may want to even drop by and say “Hey.” This will be a “dry run” broadcast to make sure all equipment is functional before the “OFFICIAL” BROADCAST SUNDAY NOVEMBER 22nd, TIME: TBA. Be sure you’re following me on PERISCOPE @IAmCoachAndrea or you can find me at The Financial Hack. I CAN’T WAIT TO CHAT WITH YOU!!!

MOTIVATION MONDAY: Plants Can Teach Lessons Too?

Let me share some Wisdom that was laid upon me early yesterday morning.

Look at this photo. In it you will see a potted plant next to the fireplace. What’s the big deal? I’ll tell you. This is the plant given to me to take care of when my cousin “Bubba” died in 2010, approximately SEVEN days after I got married. I married Christmas Eve, he passed New Year’s Eve. Five years later, his plant is still thriving but that wasn’t always so. I always took special care of that particular plant. I watered and pruned it. After a while it was no longer thriving. It began to wither, the leaves became sparse and I could tell it was dying. After a while, I thought there was no hope left for “Bubba’s plant,” but I refused to let it go. Bubba was like a little brother to me and when he was a young boy, like a son. 24 years old is too young to die and he had so much living to do.

So what happened to the plant you ask? There’s an answer to that too. I evaluated the factors contributing to the death of the one plant I cherished so much and came to three conclusions:

1) The plant had been in the same spot receiving DIRECT sunlight for years. All plants don’t need direct sunlight they just simply need to be in the “presence” of the light.

2) The leaves were yellowing because of overwatering but I couldn’t understand why its growth had become stunted and wasn’t thriving.

THEN WHAT WAS MOST IMPORTANT HIT ME:

3) THE PLANT HAD OUTGROWN IT’S PLANTER!!! Its roots were exposed and could no longer spread because its soil had eroded.

To solve the problem, I re-potted the plant into a planter that could accommodate its growth, added more soil to COVER its roots and repositioned the plant so it was no longer receiving direct sunlight. The result: ABUNDANT GROWTH. The new planter not only made room for the roots to spread and grow, but old leaves were revived, new leaves formed and as I type this, sprouts of new leaves can be seen.

So what did I learn from my quiet time in reflection:

In life, we sometimes have to be “RE-POTTED,” our roots “RE-COVERED” and our life “REPOSITIONED” in order to thrive.

Change is inevitable. We can adapt to it or resist and risk stunting our growth. I could have given up on “Bubba’s plant,” but I refused. Look at it now. Growing. Thriving. Flourishing. THAT’S LIFE. THAT’S LIVING.

Rest In Peace Bubba…. I Love You.

The Financial Hack ©2015

NOW ON PERISCOPE

Live Broadcast…. COMING SOON!!! You’ve READ my postings on my website, now SEE AND LISTEN to what I have to say via Periscope. Follow me at: The Financial Hack. See you there!!!

TIP TUESDAY: HACKS FOR THE HOME BUYER

Purchasing a home for most first-time buyers is a wonderful feeling. It’s a sense of accomplishment like no other. No more apartment living, and no more renting. For some a home purchase is seen as a place to start or raise a family. For some, it’s seen an investment. For others, it’s seen as BOTH. Going through the home-buying process can be quite stressful. Presenting W-2’s, check stubs, bank statements, tax returns, paying earnest money, scheduling a home inspection and negotiating with the seller can be overwhelming, but in the end after signing that 1 1/2″ stack of papers at closing and getting the keys to YOUR NEW HOME, you can now breathe a sigh of relief. Here are just a few tips for the FIRST TIME HOME BUYER.

- KNOW WHERE YOU STAND REGARDING YOUR CREDIT SCORE: Before you start “looking” for a home, start with obtaining a copy of your credit report. Know your credit score. This will ultimately determine if you qualify for a low interest rate (because of a good credit score) or “subprime” interest rate (because of a lower credit score.) In some cases where a couple, for instance, is purchasing a home together, if the credit score of one of the applicants will in some way negatively affect the application process (i.e. resulting in a higher interest rate,) your loan officer will usually suggest removing him or her all together from the loan application. Also, take this time to “clean up your credit.” Perhaps you have some 30, 60 or 90 day late payments within the past year. This can ultimately impact your credit score and possibly ruin your chances of obtaining any type of financing. Dispute anything on your credit report that may be incorrect such as judgements/liens, etc., and PLEASE PLEASE PLEASE make sure you are current on your student loan payments. I suggest to anyone who may have a few minor bumps and bruises on their credit report to take 1-2 YEARS to make monthly payments ON TIME on all installment accounts/loans and dispute any incorrect information on your credit report. This time can also be taken to save up a down payment, add to your existing down payment, or save additional monies for any upgrades (painting, carpet, etc.,) that may not be included in negotiations. GOOD RULE OF THUMB: If you have any credit card debt, take the time to eliminate it FIRST before making plans to purchase your dream home.

- KNOW HOW MUCH HOME YOU CAN AFFORD: There is absolutely NO POINT in looking at homes in the $200K+ range when you now you should be looking for a home in the $120-$150K range. Bank websites will allow you to plug in information such as income, minimum payment on credit card debts, installment loans, etc., and produce what is called a “prequal” (prequalification) letter but beware. Most people like to “stretch the truth” when it comes to providing certain information online, and although some real estate agents won’t show homes in certain price ranges without one, it’s best to obtain a prequalification letter from your loan officer. The loan officer can provide a more accurate picture of how much house you can actually afford. As a good rule of thumb, your mortgage payment should be 28-36% of your monthly income (given certain circumstances.)

- KNOW WHAT YOU ARE LOOKING FOR IN A HOME: Most people do their research before they even contact a Real Estate Agent/Broker. Websites such as Trulia (http://trulia.com) and Zillow (http://zillow.com) can provide listings of homes which include listing price, photos, even the MLS number that you can pass along to your Agent. It’s important to have an idea of what you’re looking for when purchasing a property. Is this a starter home? An investment property? What city? Subdivision? Are you looking for a home large enough for a growing family? What about the local school district? Proximity to shopping/retail? How close are you to the nearest freeway/major thoroughfare? How many bedrooms do you require? Is a gourmet kitchen a necessity? A large Master Bedroom/Bath? What about a Game/Media Room? A Study perhaps? A Pool? These are decisions you need to make BEFORE meeting with an agent because your agent will ask the same questions (and I’ll bet you dollars to donuts they’re fingers are crossed upon your initial meeting and/or phone conversation, you already know what your looking for.) FYI: It has been my experience in the Real Estate industry Kitchens and Bathrooms are huge sellers for women. For men, as long as there is a dedicated “man cave” in the home that is all his and he can decorate it any way he chooses, he’ll usually go along with whatever his partner/spouse wants.

- KNOW WHAT TYPE OF LOAN IS BEST FOR YOU: I won’t get into loan specifics (I’ll save that for a later posting,) but the Conventional home loan is your best bet. Most lenders assume a 30-year fixed mortgage is what is desired, but inquire about a 15-year fixed rate mortgage. You’ll get a better interest rate, although your mortgage payment will be higher, but you’re also taking less time to pay the loan off. FHA loans are advantageous to the buyer who doesn’t have a large down payment plus the debt-to-income ratio requirements are a little more lax than conventional loans. VA loans are great for Veterans because no down payment is required. Beware however of seller fees. Whether a VA loan is granted depends on the length of time on active duty and the number of past VA loans. STEER CLEAR OF THE FOLLOWING LOANS: ARMs (Adjustable rate Mortgages,) Interest Only Loans and Reverse Mortgages.

- KNOW HOW MUCH MONEY YOU PLAN TO HAVE AS A DOWN PAYMENT: After the housing market crash in 07-08, regardless of how excellent your credit score was, some lenders began requiring a 20% down payment. The good thing about putting down 20% is in some cases it exempts the buyer from paying what is called PMI (Private Mortgage Insurance.) If PMI is being paid on your home, if you can demonstrate the home has accumulated a certain amount of equity in it (20% if I’m not mistaken,) the $50-120/mo that is being paid can be removed. What’s ironic about PMI is some buyers believe PMI protects them… WRONG! PMI protects the lender in case the buyer defaults on making payments.

- ALWAYS DO YOUR DUE DILIGENCE: The performance of local school districts is one of the main factors potential home buyers pay close attention to whether they have children, intend to have children or have no children. A school district’s rating with the state can positively or negatively impact the desirability of a home and for some buyers can be a “deal breaker.” Also it is up to the buyer to do their due diligence regarding sex offenders who may be living in the neighborhood or residing nearby.

- ALWAYS HAVE A QUALIFIED HOME INSPECTION PERFORMED: As the saying goes, NEVER JUDGE A BOOK BY ITS COVER. A home may look good on the outside and even on the inside, but the home could be a potential health hazard. Faulty wiring, signs of mold that an untrained eye may not detect, pipe leaks underneath the home, and the infamous “foundation issues” can result in costly repairs all of which aren’t always covered by your insurance carrier.

- ALWAYS ANTICIPATE INCURRING ADDITIONAL COSTS WHEN IT COMES TO HOME AMENITIES/UPGRADES: Take into consideration the size of your home and how many A/C units the home will have. A 4000+ square foot home will have at minimum TWO units. And if you’re running both units in the summer, just wait until you get that first electric bill. Does your home have an in-ground swimming pool? If it does, guess what? The pool isn’t going to clean and maintain itself which means either you’ll have to do it yourself or hire someone to do it for you. Even if you choose to maintain the pool on your own, the chemicals aren’t cheap, however doing it yourself will still save money.

- CHOOSE A KNOWLEDGEABLE REAL ESTATE AGENT/BROKER: This is self explanatory. Find a realtor who is familiar with the area(s) you’re looking to purchase a home in. They should have “Comps and Analysis” of homes in your price range and with similar amenities that have sold recently in the area. An Agent/Broker may be working with multiple clients at a time, but that is no excuse for poor customer service. That person is working for you and you deserve nothing less than the best buying experience. Never allow an agent pressure you to make an offer on a home you’re uncertain about it. When you find the “right home,” you’ll know. Trust me on this one.

- MAKE SURE YOUR HOME IS PROPERLY INSURED: The worst thing that can happen if a catastrophic event occurs (God forbid) is that the homeowner is “underinsured.” Always check with your insurance provider to make sure you are properly insured. Start with the company that insures your vehicles. Insurance companies such as State Farm, Allstate, Nationwide, Farmers, etc. will usually provide a discount for allowing them the privilege to get that additional commission (cough cough,) I mean insuring your property as well. Shop around to make sure you’re getting the best rate. It’s also a good idea each year to make an appointment with your insurance agent to review your policy and make any changes if necessary.

Although this posting was quite lengthy, the information given should get you started on your quest to a successful home buying experience. CONGRATULATIONS…YOU ARE ON YOUR WAY!!!!

Please feel free to leave any and all comments below. If you have a specific question, email me at Andrea.Coleman@TheFinancialHack.com.

~The Financial Hack ©2015

FINANCIAL FITNESS BOOT CAMP WEEK 10: WHAT’S ALL THE “BROUHAHA” ABOUT MY FICO SCORE ANYWAY?

Credit score this, FICO score that. Blah Blah Blah. Our ability on whether credit is extended to us (or not) can hinge on our FICO/Credit score. What is a Credit/FICO Score? Why is it so important? Some of you may be reading this and thinking, “I already understand credit, it’s importance and how it works.” If you are that person, that’s great. This post isn’t for you. This posting is for the person who doesn’t know what a FICO score is, doesn’t quite understand the importance of the FICO/Credit score, how to mange credit responsibly and how it can impact variables such as interest rates on loans (home, car etc.,) whether additional credit will be extended to you, whether a deposit is required for certain utilities, whether you’re in contention for a job offer, and even car insurance rates. How is it that an insurance underwriter is able to assume because someone’s credit score is fair/poor they are prone to being involved in more car accidents or more susceptible to irresponsible/reckless driving? The same holds true for a potential employer who dismisses an applicant because their credit score is “less than stellar.” Is the employer taking into consideration WHY a person’s credit score is what they deem to be “less than stellar” when making the selection process even though the applicant is qualified for the job? These are serious questions that require serious answers, but let’s not get ahead of ourselves. Let’s first understand what a FICO/Credit Score is.

FICO score and Credit score are usually used interchangeably. Most people call it your “Credit Score” but allow me to give you a bit of background on what the term FICO stands for and what it consists of.

FICO was founded in 1956 as “Fair, Isaac and Company” hence the name FICO by engineer William Fair and mathematician Earl Isaac. The two met while working at the Stanford Research Institute in Menlo Park, CA. Selling its first credit scoring system two years after the company’s creation, FICO pitched its system to fifty American lenders.

FICO went public in 1986 and is traded on the New York Stock Exchange. The company debuted its first general-purpose FICO score in 1989. Scores are based on credit reporting and range from 300 to 850. (Historical information taken from Wikipedia.)

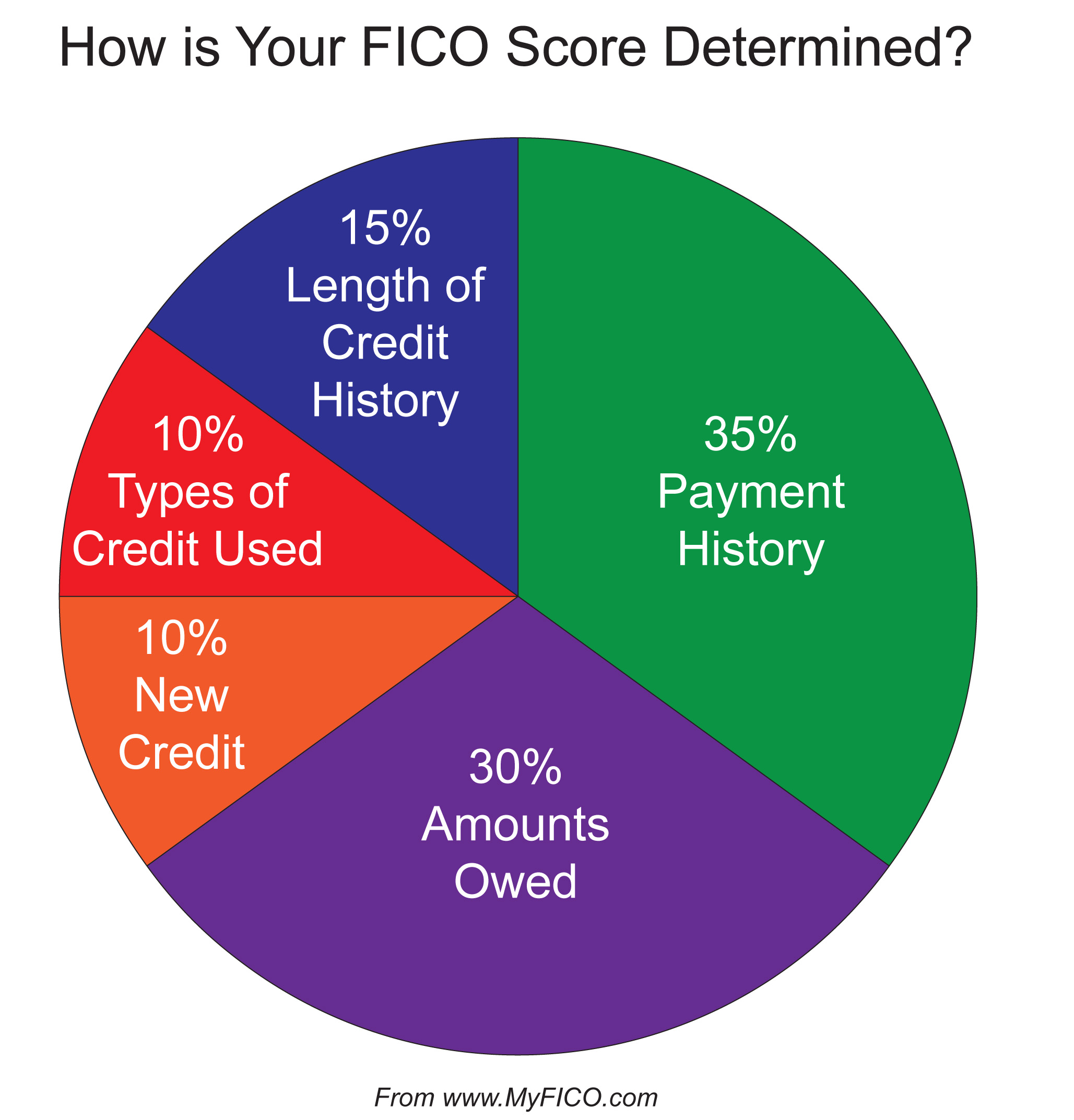

Lenders use FICO scores to gauge a potential borrower’s creditworthiness. Scores are provided by the three credit bureau reporting agencies, Experian, Equifax and TransUnion. There are FIVE components that make up a person’s FICO/Credit score.

- Payment History (35%)

- Debt/Amounts Owed (30%)

- Length of Credit History (15%)

- New Credit/Inquiries (10%)

- Types of Credit (10%)

FICO SCORE BREAKDOWN:

The two categories of the five that are the most important are Payment History (how long you’ve had your credit account(s) such as a credit card) for instance, and Amounts Owed (debt-to income.) Be careful of “maxing out” credit cards or keeping a balance that is too close to your credit limit. As a good rule of thumb, your credit balance SHOULD NOT exceed 50% of your credit card’s limit. Any balance above 50% of your credit limit can actually lower your credit score. It’s always good to have a good mix of credit: Installment Credit (home/car loans,) Revolving Credit (credit cards,) Charge Credit (the balance is due IN FULL at the end of the month) and Service Credit (Utilities, gym memberships, etc.) NOTE: Service credit is not always reported to credit bureaus however a letter can be provided to a potential creditor by the company if necessary.

Having a good credit score can get you better interest rates on homes, cars and even credit cards whereas less than stellar credit will yield higher rates simply because the risk to the lender is much greater.

NOW LET’S GET TO THE NITTY GRITTY…..

A lot of people brag about having a good credit score and having a good credit score is certainly important but please bear this in mind: A CREDIT SCORE IS MERELY AN INDICATOR TO THE LENDER OF HOW WELL A PERSON CAN HANDLE DEBT. I know people who have EXCELLENT credit scores but are up to their eyeballs in debt. A high credit score IS NOT an indicator of wealth. It simply means some people are better managers of their debt. A person with a good credit score can look great on paper, but in some cases that’s pretty much the extent of it.

Now let’s take a look at the person who has a fair/poor credit score. Bankruptcy, divorce, unemployment, disability, medical issues, or death of a loved one are among many factors that can play a role in a declining credit score. Don’t misunderstand me. Irresponsibility, immaturity, mismanagement and just plain ole ignorance are culprits as well. Before you discredit the person who has a fair/poor credit score, find out why. We automatically assume it’s because the person is irresponsible, immature or even broke. Think again.

FICO SCORES ARE INTERPRETED A LITTLE SOMETHING LIKE THIS:

You are entitled to one FREE copy of your credit report. Go to http://www.MyFreeCreditReport.com to order yours. If you are denied credit for any reason, the lender/creditor is required to inform you (via letter) their reason(s) for making their decision. You are then given a report number you can use to access a copy (free of charge) of your credit report as well. IT’S IMPORTANT TO KNOW WHERE YOU STAND.

I hope this posting gave you some introductory insight regarding credit and how it works. Next week we’ll delve a bit deeper into how to read a credit report, what can help your credit score, what can hurt your credit score and ways you can improve your credit score. YES, YOU CAN REPAIR YOUR OWN CREDIT!!!

As always, I appreciate you taking the time to read this posting. Feel free to comment below. If you have any direct questions, email me at Andrea.Coleman@TheFinancialHack.com.

~The Financial Hack ©2015

DAILY MOTIVATION

When your money game is as strong as your wifi connection… #GoalDiggersDFW

HACKS FOR THE LANDLORD

They say the path to millionaire status can be obtained by becoming a landlord. “Buy land,” they say. “That’s something they aren’t making any more of.” I have more than a couple of investment properties and I’m far from millionaire status but I’m on my way. Check with me in about 15 years and we’ll see how close I am.

Since my last “Tip Tuesday” blog posting “Hacks for Tenants/Renters,” I thought I would follow up with “Hacks for Landlords.”

READ MY HACKS FOR TENANTS/RENTERS HERE:

https://thefinancialhack.com/2015/10/20/tip-tuesday-hacks-for-tenantsrenters/

Based on my 10+ years of experience being a Landlord and Property Manager, I’ve learned “what to do” and “what not to do” when it comes to “Landlording.” Just as the tips for tenants proved useful (at least I hope they did,) these hacks should prove useful to the Landlord as well. For all practical purposes, I’ll be speaking to those who own and/or manage Single Family Dwellings.

- ALL RENT IS NEGOTIABLE: Just as I mentioned “All Rent is Negotiable” in the Hacks for Tenants/Renters posting, obviously the same goes for Landlords on the flip side of the coin. Some Landlords are firm on their asking price, however, depending on the level of motivation, an Owner may be willing to bend slightly on the rent. When you think about it, if you’re talking about a difference of $50-100, it’s worth it to negotiate and find a middle ground, especially if you think you’ve found the perfect tenant.

- NEVER JUMP ON THE FIRST TRAIN SMOKING: This is the biggest mistake I see new Landlords make. The Landlord is so eager to lease the home and because the potential tenant(s) look good on paper, have the deposit and first month’s rent and “appear” to be “really nice,” the Landlord rents to that potential tenant in haste. The rest of the story in some cases is a complete disaster!

- POTENTIAL RED FLAGS: These are some of my personal favorites: 1) The potential tenant who has the deposit/first month’s rent, will do the once over of the property, complete the lease application on site, run to 7-Eleven, get a money order for the app fee(s), brings everything back to you within 30 minutes, (this could be on a Monday no doubt,) and expects a Friday move in. WHAT!!!! THOSE VERY ACTIONS SIGNAL TO ME A TENANT THAT IS ABOUT TO SKIP OUT ON PAYING RENT WHERE HE/SHE/THEY CURRENTLY RESIDE. If they’ll skip out on a previous Landlord, they’ll do the same to you. Beware. This is not always the case, but in my experience RUN FOR THE HILLS!!! Nine times out of ten, it is. I require a copy of a Driver’s License/ID Card, Social Security Card, Utility Bill (to verify current address) and the most recent check stub. Some may believe I’m asking for too much information, but this is actually a part of the “weeding out” process. If a potential tenant doesn’t feel it necessary to provide me with the information I require, another one will come along who has no problem doing so. 2) The potential tenant, who after reviewing the Residential Lease Application informs you for the last FIVE YEARS of residential history (which is what I ask for) they lived with a sick relative usually a mother or father. I always find it comical when this happens because I’ll ask them to go back another five years, and I’ll usually get another relative they lived with or another type of excuse. Bad rental history is better than no rental history: It may be shaky, but at least a Landlord knows where an applicant stands.

- WHEN SHOWING YOUR PROPERTY TO A POTENTIAL TENANT, TREAT IT AS AN INTERVIEW PROCESS: I hate to say it, but APPEARANCE DOES MATTER. Your potential tenant doesn’t have to dress as if they’re interviewing for a Fortune 500 Company, however, they shouldn’t look like they just rolled out of bed to meet you either. Don’t discount potential tenants because of their looks, but do pay attention. Ask questions and observe their behavior. You can learn a lot just by asking simple questions such as where they work. Ask them to explain what it is they do. Ask about their family (or how many will be occupying the property) especially if a person comes alone to view the property. Also, take notice whether the potential tenant is on time or late. I try to arrive at the property 15-20minutes before the scheduled time to make sure I greet them when they arrive. In some cases, I have had potential tenants arrive at the property before I did even though I arrived early. Nothing looks worse than a Landlord/Property Manager who is late to their own showing. If a tenant hasn’t contacted me to inform me they’re running late, I give them 20 minutes tops, and I lock up and leave. Time is a valuable commodity that is not to be wasted.

- ALWAYS PROTECT YOURSELF: If you can, have another person present when you are showing a property. If you are alone, arrive early (you should do that anyway) and wait outside while the potential tenant views the property. I usually have protection (if you know what I mean) whether someone is with me or not, however I still wait outside.

- HAVE YOUR TENANT COMPLETE A RESIDENTIAL LEASE APPLICATION: Make sure it includes the necessary questions including bankruptcy, foreclosure, judgements/liens, evictions and my personal favorite: HAVE YOU EVER BROKEN A LEASE FOR ANY REASON? If yes, please explain. The application should have the potential tenant list their social security number, employment history, past rental/purchase history, previous addresses (5 years,) number of occupants, vehicles, you get the picture. Ask them to explain any evictions, judgements/liens and bankruptcies. Some tenants will be forthright with any potential damaging information, others will allow you to find out on your own. The last page of the application is a signature page where the potential tenant attests the info included in the application is factual and correct and their signature authorizes you to access their credit report as well as verify employment/rental history.

- ALWAYS PULL A CREDIT REPORT: In a nutshell, a person’s credit (FICO) SCORE will tell me how well they can manage debt. NEVER RELY SOLELY ON A CREDIT SCORE TO DETERMINE WHETHER A POTENTIAL TENANT WILL BE A “DEAL” OR A “DUD.” As I stated in my Hacks for Tenant/Renters posting, my BEST tenant of 8 years (and counting) had an initial credit score of 505 and has NEVER been late on the rent. The tenant was forthright in disclosing her financial situation upon our initial meeting. That spoke volumes on her behalf.

- MAKE SURE YOU HAVE A “THOROUGH” LEASE AGREEMENT: The lease agreement should not only protect you the Landlord, but it should also protect the tenant as well. Become familiar with your state laws regarding Landlord/Tenant relationships. If you have certain rules regarding your property (such as no smoking,) it must be expressed, not implied. Stipulate your rules in the lease. If no pets of any kind are allowed on the premises (this includes fish, gerbils, snakes, iguanas llamas, flies, giraffes, gazelles, monkeys, and zebras…Oh and dogs and cats too,) be sure to specify that in the lease as well. Some tenants have to have it spelled out. Be as specific as necessary in order to cover your “assets.” Information regarding rent grace periods, late fees, the eviction process, and even procedures to place a work/repair order must be included as well. Leave no stone unturned.

- STRESS TO YOUR NEW TENANT THE IMPORTANCE OF SECURING RENTERS INSURANCE: If the home is destroyed by some catastrophic event, the insurance on the property covers the structure ONLY, not the contents inside. By law, as a Landlord, you can’t insure property that doesn’t belong to you. The cost is relatively inexpensive (apprx. $10-$12 for about $20K of coverage.) It’s always better to be safe than sorry.

- NEVER “COMMINGLE” YOUR MONEY WITH THE TENANT’S DEPOSIT: All security deposits should be kept in a separate escrow account.

- TAKE PHOTOGRAPHS AND VIDEO OF THE PROPERTY PRIOR TO THE TENANT’S MOVE-IN DATE: Do the same once a tenant vacates the property as well. Make sure the picture and video is date/time stamped. This is a little “insurance policy” in case you have to prove or defend your case in court.

- WHEN DEALING WITH REPAIRS, YOUR RESPONSE TIME AS A LANDLORD IS EVERYTHING: A prompt response to the Tenant builds trust between the Landlord/Property Manager and the Tenant. My response time is usually the same day and in most cases the issue is resolved within 24-48 hours. I answered a call while vacationing in Canada for a few days. THAT’S TOP NOTCH CUSTOMER SERVICE!! Always have an “Elite Team” of dependable repairmen (licensed and bonded) that you can contact when necessary. Let the Tenant know SPECIFICALLY the procedure(s) to follow when placing a work order/repair request. Now when I vacation, I inform all Tenants the duration of my vacation and who they are to contact in the case of an emergency.

- PREVENTATIVE MAINTENANCE CAN SAVE A LANDLORD COSTLY REPAIRS IN THE LONGRUN: Routine maintenance (HVAC, Electrical, Plumbing, Even Yearly Extermination/Pest Control) can save you money down the road. Just as you schedule routine maintenance on your vehicle, performing routine maintenance on your properties serves the same purpose.

- STRESS TO THE TENANT THE IMPORTANCE OF SCHEDULING A “WALK-THROUGH PRIOR TO THEM VACATING THE PREMISES: By doing this, the tenant isn’t caught off guard by deductions taken from the security deposit.

- IF RENTING TO FRIENDS/FAMILY MEMBERS LET THEM KNOW IT’S BUSINESS… NOTHING PERSONAL: Beware of friends/family members who may attempt to take advantage of your relationship. Think long and hard if you believe the relationship may be damaged if things go south.

- JOIN ORGANIZATIONS SUCH AS THE LPA (LANDLORD PROTECTTION AGENCY): This organization has helpful information for Landlords, sample leases and most importantly, the ability to run credit checks on potential tenants for a nominal fee. It’s wise to take advantage of these types of organizations. A one year membership to the LPA is less than $100. Visit their website at http://www.theLPA.com

- If “all of the above” seems like too much of a headache for you, find an “experienced” Property Manager to take away the hassle of “Landlording.” A Property Manager will charge you a monthly fee, which is usually a percentage of the rent collected. MAKE SURE THE PROPRTY MANAGER YOU SELECT IS SOMEONE YOU CAN TRUST TO GET THE JOB DONE. Real estate agencies provide these services as well as independent brokers such as myself. Always do your due diligence when making your selection. Years of experience, number of properties managed and knowledge of the state’s law regarding Landlord/Tenant relationships is a great place to start.

There are so many additional tips for the Landlord I could have included. Perhaps I’ll save my additional Landlord tips and anecdotal stories for my second book (after I write the first one.) Hopefully these tips will get you started if you’re new to the world of “Landlording.” If you have any questions, or would like additional information, email me at AndreaColeman@TheFinancialHack.com. Feel free to leave your comments and feedback below and as always thank you for reading.

~The Financial Hack (copyright 2015)

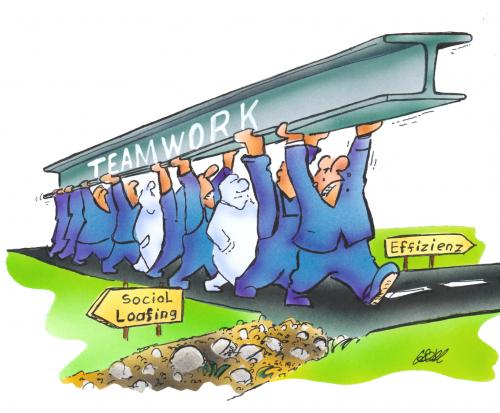

EACH ONE TEACH ONE MOMENT: THE IMPORTANCE OF TEAMWORK

With me trying to adjust to this new “work schedule” of mine, I had no intention of actually writing any posts this week, but I felt compelled to do so today… This will be one of my “Each One Teach One” postings, and I’ll use football, (yep football) as an example. Now c’mon. Did you expect anything different?

I wrote a few weeks ago about Madden Mobile, a FREE mobile app in a previous posting. Feel free to read about it here:

Now some of you may be thinking: Why on earth is a forty-something year old female wasting her time playing video games? I don’t consider myself a “gamer,” but I do play video games to decompress and unwind. And, also because they’re fun, but I digress. What does Madden Mobile have to do with teamwork? Allow me to extrapolate (Oooo an SAT word, lol).

One great aspect about Madden Mobile, is you can connect with people across the country by joining a league. You can request to join a league, a league can scout you (as in my case,) or you can even start your own. Still, what does that have to do with teamwork you may be asking… EVERYTHING!!! I could have continued to play alone but there are advantages to playing in a league. Comradery is what I enjoy the most. You can chat with other league members and/or give the team encouragement via the league chat board. We played rival teams, and we played each other for fun. We were a team… or so I thought. Our teamwork photo at the moment looks something like this:

WHY? EVERY MEMBER IS NOT HOLDING THEIR WEIGHT…

All this time I’ve been playing with this particular league, I thought we were all working together, winning as a team, and for a time, it felt as though we were a team… Until we started losing. Once we started losing, it seems as though collectively, “the team” had completely given up on the vision. The vision to win.

Playing football is similar to playing chess. The object is to win obviously, however, there is an objective even greater than the win itself: Outsmarting your opponent by anticipating their next play and stopping them from advancing. In Madden, I get more of a rush from outsmarting my opponents by switching up plays than scoring actual touchdowns.

Football requires TEAMWORK for a reason. Where one team member may be weak in a particular area, another team member may be stronger and can pick up the slack. In a case where it’s obvious your team might lose, YOU DON’T GIVE UP. THAT’S WHEN YOU COME TOGETHER AS A TEAM AND FIGHT HARDER!!! And you fight until the clock says zero. You don’t stop playing with 4:52 seconds left in the 3rd quarter because the score is 35-0. You use that deficit as your motivation to try harder. It upsets me when I see people giving up because they’re losing. That’s life. Don’t get mad, pick up your marbles and go home because you’re not winning. KEEP PLAYING! It can only develop you and make you better. And if you lose, the next time you face an opponent, you’ll be ready. Don’t doubt yourself and turn away because you’re facing an opponent you DON’T BELIEVE you can defeat. You won’t know until you try. I can’t tell you how many opponents on the field/obstacles in life I thought would get the best of me, but I refused to give up. When you give up, not only are you disappointed in yourself because you’re losing/lost, but you’ve disappointed those teammates/the people that believed in the vision, the win, and refused to give up in spite of an anticipated loss. I have more respect for a fellow team member who tried but didn’t score, than a person who quit before the game/fight was over. This could be the fight to win in your finances, marriage/relationships, the workplace, your organization, or even in your church. As a team, in order to claim victory, you must work together and never give up!

If a team worked together as one single solitary unit as opposed to the “every man for himself” attitude, just imagine what could be accomplished. Your teamwork photo would probably look more like this:

…. AND EVERYONE WINS!!!

Remember, “There is no “I” in team.”

That cliche’ will NEVER get old… At least not to me.

~The Financial Hack ©2015

MOTIVATION MONDAY: PARKING LOT ATTENDANT WORTH $500K

It’s not about how much you make, it’s what you do with what you make that counts.

~The Financial Hack