Credit score this, FICO score that. Blah Blah Blah. Our ability on whether credit is extended to us (or not) can hinge on our FICO/Credit score. What is a Credit/FICO Score? Why is it so important? Some of you may be reading this and thinking, “I already understand credit, it’s importance and how it works.” If you are that person, that’s great. This post isn’t for you. This posting is for the person who doesn’t know what a FICO score is, doesn’t quite understand the importance of the FICO/Credit score, how to mange credit responsibly and how it can impact variables such as interest rates on loans (home, car etc.,) whether additional credit will be extended to you, whether a deposit is required for certain utilities, whether you’re in contention for a job offer, and even car insurance rates. How is it that an insurance underwriter is able to assume because someone’s credit score is fair/poor they are prone to being involved in more car accidents or more susceptible to irresponsible/reckless driving? The same holds true for a potential employer who dismisses an applicant because their credit score is “less than stellar.” Is the employer taking into consideration WHY a person’s credit score is what they deem to be “less than stellar” when making the selection process even though the applicant is qualified for the job? These are serious questions that require serious answers, but let’s not get ahead of ourselves. Let’s first understand what a FICO/Credit Score is.

FICO score and Credit score are usually used interchangeably. Most people call it your “Credit Score” but allow me to give you a bit of background on what the term FICO stands for and what it consists of.

FICO was founded in 1956 as “Fair, Isaac and Company” hence the name FICO by engineer William Fair and mathematician Earl Isaac. The two met while working at the Stanford Research Institute in Menlo Park, CA. Selling its first credit scoring system two years after the company’s creation, FICO pitched its system to fifty American lenders.

FICO went public in 1986 and is traded on the New York Stock Exchange. The company debuted its first general-purpose FICO score in 1989. Scores are based on credit reporting and range from 300 to 850. (Historical information taken from Wikipedia.)

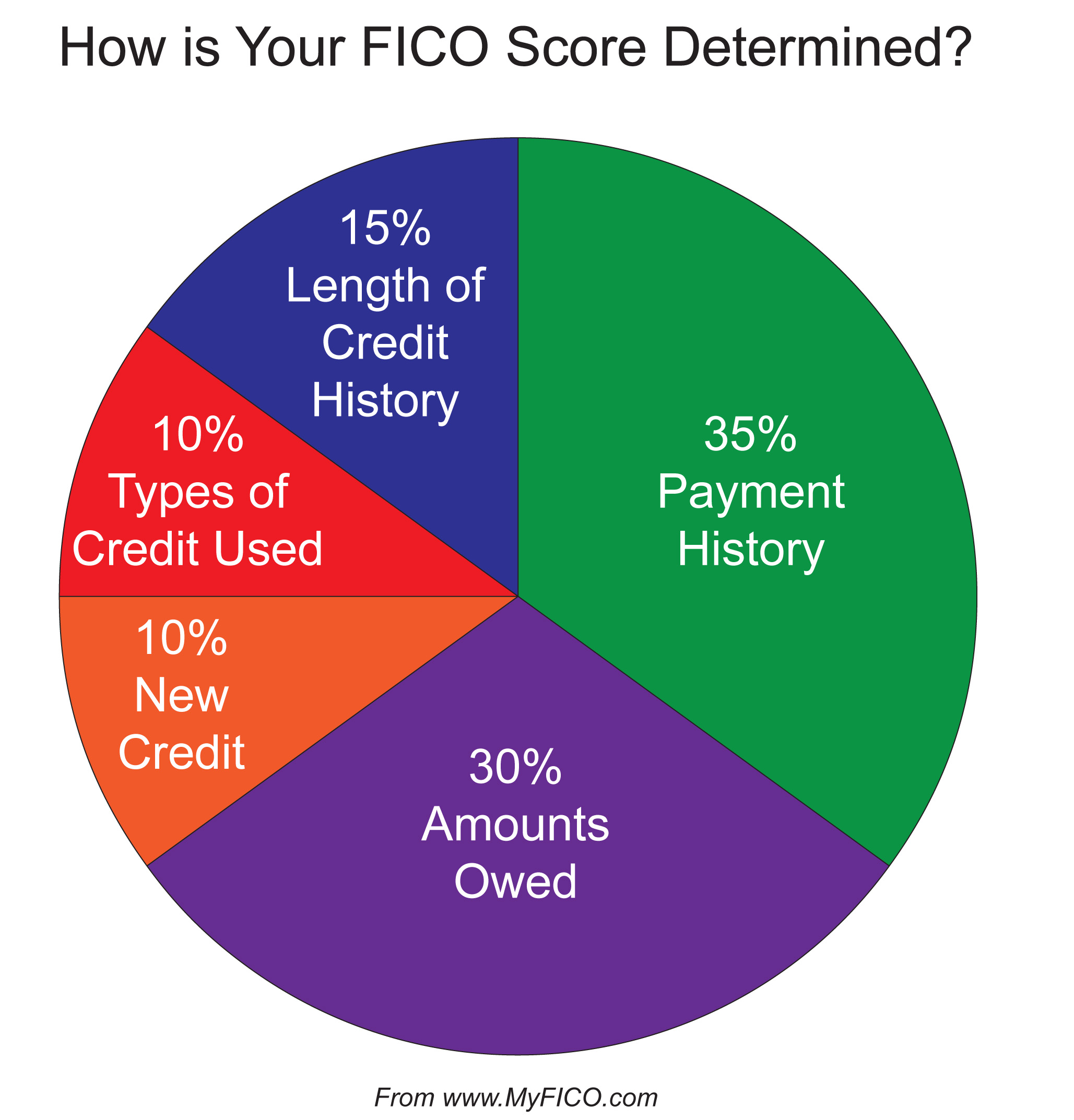

Lenders use FICO scores to gauge a potential borrower’s creditworthiness. Scores are provided by the three credit bureau reporting agencies, Experian, Equifax and TransUnion. There are FIVE components that make up a person’s FICO/Credit score.

- Payment History (35%)

- Debt/Amounts Owed (30%)

- Length of Credit History (15%)

- New Credit/Inquiries (10%)

- Types of Credit (10%)

FICO SCORE BREAKDOWN:

The two categories of the five that are the most important are Payment History (how long you’ve had your credit account(s) such as a credit card) for instance, and Amounts Owed (debt-to income.) Be careful of “maxing out” credit cards or keeping a balance that is too close to your credit limit. As a good rule of thumb, your credit balance SHOULD NOT exceed 50% of your credit card’s limit. Any balance above 50% of your credit limit can actually lower your credit score. It’s always good to have a good mix of credit: Installment Credit (home/car loans,) Revolving Credit (credit cards,) Charge Credit (the balance is due IN FULL at the end of the month) and Service Credit (Utilities, gym memberships, etc.) NOTE: Service credit is not always reported to credit bureaus however a letter can be provided to a potential creditor by the company if necessary.

Having a good credit score can get you better interest rates on homes, cars and even credit cards whereas less than stellar credit will yield higher rates simply because the risk to the lender is much greater.

NOW LET’S GET TO THE NITTY GRITTY…..

A lot of people brag about having a good credit score and having a good credit score is certainly important but please bear this in mind: A CREDIT SCORE IS MERELY AN INDICATOR TO THE LENDER OF HOW WELL A PERSON CAN HANDLE DEBT. I know people who have EXCELLENT credit scores but are up to their eyeballs in debt. A high credit score IS NOT an indicator of wealth. It simply means some people are better managers of their debt. A person with a good credit score can look great on paper, but in some cases that’s pretty much the extent of it.

Now let’s take a look at the person who has a fair/poor credit score. Bankruptcy, divorce, unemployment, disability, medical issues, or death of a loved one are among many factors that can play a role in a declining credit score. Don’t misunderstand me. Irresponsibility, immaturity, mismanagement and just plain ole ignorance are culprits as well. Before you discredit the person who has a fair/poor credit score, find out why. We automatically assume it’s because the person is irresponsible, immature or even broke. Think again.

FICO SCORES ARE INTERPRETED A LITTLE SOMETHING LIKE THIS:

You are entitled to one FREE copy of your credit report. Go to

http://www.MyFreeCreditReport.com to order yours. If you are denied credit for any reason, the lender/creditor is required to inform you (via letter) their reason(s) for making their decision. You are then given a report number you can use to access a copy (free of charge) of your credit report as well.

IT’S IMPORTANT TO KNOW WHERE YOU STAND.I hope this posting gave you some introductory insight regarding credit and how it works. Next week we’ll delve a bit deeper into how to read a credit report, what can help your credit score, what can hurt your credit score and ways you can improve your credit score. YES, YOU CAN REPAIR YOUR OWN CREDIT!!!

As always, I appreciate you taking the time to read this posting. Feel free to comment below. If you have any direct questions, email me at Andrea.Coleman@TheFinancialHack.com.

~The Financial Hack ©2015