Purchasing a home for most first-time buyers is a wonderful feeling. It’s a sense of accomplishment like no other. No more apartment living, and no more renting. For some a home purchase is seen as a place to start or raise a family. For some, it’s seen an investment. For others, it’s seen as BOTH. Going through the home-buying process can be quite stressful. Presenting W-2’s, check stubs, bank statements, tax returns, paying earnest money, scheduling a home inspection and negotiating with the seller can be overwhelming, but in the end after signing that 1 1/2″ stack of papers at closing and getting the keys to YOUR NEW HOME, you can now breathe a sigh of relief. Here are just a few tips for the FIRST TIME HOME BUYER.

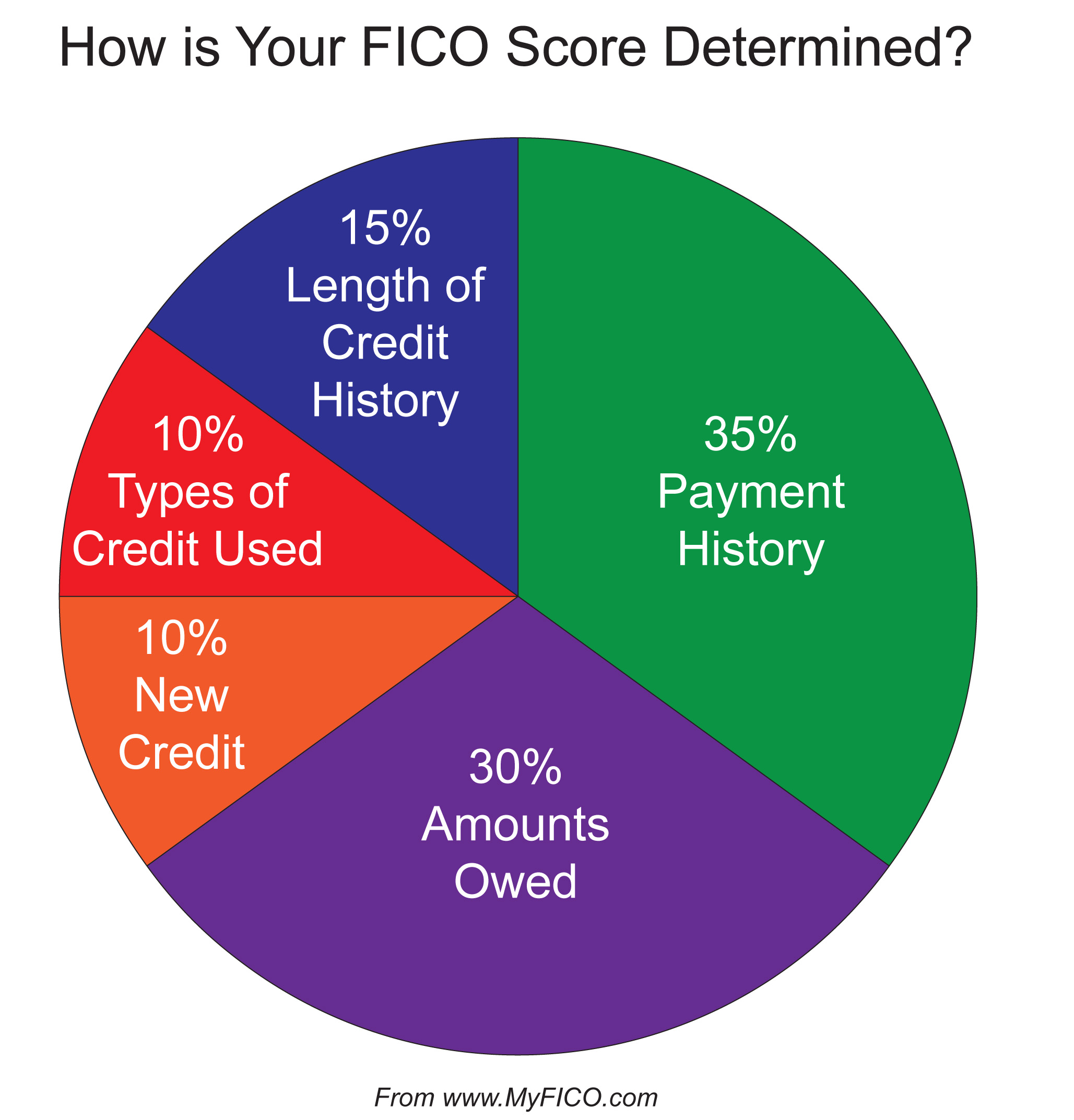

- KNOW WHERE YOU STAND REGARDING YOUR CREDIT SCORE: Before you start “looking” for a home, start with obtaining a copy of your credit report. Know your credit score. This will ultimately determine if you qualify for a low interest rate (because of a good credit score) or “subprime” interest rate (because of a lower credit score.) In some cases where a couple, for instance, is purchasing a home together, if the credit score of one of the applicants will in some way negatively affect the application process (i.e. resulting in a higher interest rate,) your loan officer will usually suggest removing him or her all together from the loan application. Also, take this time to “clean up your credit.” Perhaps you have some 30, 60 or 90 day late payments within the past year. This can ultimately impact your credit score and possibly ruin your chances of obtaining any type of financing. Dispute anything on your credit report that may be incorrect such as judgements/liens, etc., and PLEASE PLEASE PLEASE make sure you are current on your student loan payments. I suggest to anyone who may have a few minor bumps and bruises on their credit report to take 1-2 YEARS to make monthly payments ON TIME on all installment accounts/loans and dispute any incorrect information on your credit report. This time can also be taken to save up a down payment, add to your existing down payment, or save additional monies for any upgrades (painting, carpet, etc.,) that may not be included in negotiations. GOOD RULE OF THUMB: If you have any credit card debt, take the time to eliminate it FIRST before making plans to purchase your dream home.

- KNOW HOW MUCH HOME YOU CAN AFFORD: There is absolutely NO POINT in looking at homes in the $200K+ range when you now you should be looking for a home in the $120-$150K range. Bank websites will allow you to plug in information such as income, minimum payment on credit card debts, installment loans, etc., and produce what is called a “prequal” (prequalification) letter but beware. Most people like to “stretch the truth” when it comes to providing certain information online, and although some real estate agents won’t show homes in certain price ranges without one, it’s best to obtain a prequalification letter from your loan officer. The loan officer can provide a more accurate picture of how much house you can actually afford. As a good rule of thumb, your mortgage payment should be 28-36% of your monthly income (given certain circumstances.)

- KNOW WHAT YOU ARE LOOKING FOR IN A HOME: Most people do their research before they even contact a Real Estate Agent/Broker. Websites such as Trulia (http://trulia.com) and Zillow (http://zillow.com) can provide listings of homes which include listing price, photos, even the MLS number that you can pass along to your Agent. It’s important to have an idea of what you’re looking for when purchasing a property. Is this a starter home? An investment property? What city? Subdivision? Are you looking for a home large enough for a growing family? What about the local school district? Proximity to shopping/retail? How close are you to the nearest freeway/major thoroughfare? How many bedrooms do you require? Is a gourmet kitchen a necessity? A large Master Bedroom/Bath? What about a Game/Media Room? A Study perhaps? A Pool? These are decisions you need to make BEFORE meeting with an agent because your agent will ask the same questions (and I’ll bet you dollars to donuts they’re fingers are crossed upon your initial meeting and/or phone conversation, you already know what your looking for.) FYI: It has been my experience in the Real Estate industry Kitchens and Bathrooms are huge sellers for women. For men, as long as there is a dedicated “man cave” in the home that is all his and he can decorate it any way he chooses, he’ll usually go along with whatever his partner/spouse wants.

- KNOW WHAT TYPE OF LOAN IS BEST FOR YOU: I won’t get into loan specifics (I’ll save that for a later posting,) but the Conventional home loan is your best bet. Most lenders assume a 30-year fixed mortgage is what is desired, but inquire about a 15-year fixed rate mortgage. You’ll get a better interest rate, although your mortgage payment will be higher, but you’re also taking less time to pay the loan off. FHA loans are advantageous to the buyer who doesn’t have a large down payment plus the debt-to-income ratio requirements are a little more lax than conventional loans. VA loans are great for Veterans because no down payment is required. Beware however of seller fees. Whether a VA loan is granted depends on the length of time on active duty and the number of past VA loans. STEER CLEAR OF THE FOLLOWING LOANS: ARMs (Adjustable rate Mortgages,) Interest Only Loans and Reverse Mortgages.

- KNOW HOW MUCH MONEY YOU PLAN TO HAVE AS A DOWN PAYMENT: After the housing market crash in 07-08, regardless of how excellent your credit score was, some lenders began requiring a 20% down payment. The good thing about putting down 20% is in some cases it exempts the buyer from paying what is called PMI (Private Mortgage Insurance.) If PMI is being paid on your home, if you can demonstrate the home has accumulated a certain amount of equity in it (20% if I’m not mistaken,) the $50-120/mo that is being paid can be removed. What’s ironic about PMI is some buyers believe PMI protects them… WRONG! PMI protects the lender in case the buyer defaults on making payments.

- ALWAYS DO YOUR DUE DILIGENCE: The performance of local school districts is one of the main factors potential home buyers pay close attention to whether they have children, intend to have children or have no children. A school district’s rating with the state can positively or negatively impact the desirability of a home and for some buyers can be a “deal breaker.” Also it is up to the buyer to do their due diligence regarding sex offenders who may be living in the neighborhood or residing nearby.

- ALWAYS HAVE A QUALIFIED HOME INSPECTION PERFORMED: As the saying goes, NEVER JUDGE A BOOK BY ITS COVER. A home may look good on the outside and even on the inside, but the home could be a potential health hazard. Faulty wiring, signs of mold that an untrained eye may not detect, pipe leaks underneath the home, and the infamous “foundation issues” can result in costly repairs all of which aren’t always covered by your insurance carrier.

- ALWAYS ANTICIPATE INCURRING ADDITIONAL COSTS WHEN IT COMES TO HOME AMENITIES/UPGRADES: Take into consideration the size of your home and how many A/C units the home will have. A 4000+ square foot home will have at minimum TWO units. And if you’re running both units in the summer, just wait until you get that first electric bill. Does your home have an in-ground swimming pool? If it does, guess what? The pool isn’t going to clean and maintain itself which means either you’ll have to do it yourself or hire someone to do it for you. Even if you choose to maintain the pool on your own, the chemicals aren’t cheap, however doing it yourself will still save money.

- CHOOSE A KNOWLEDGEABLE REAL ESTATE AGENT/BROKER: This is self explanatory. Find a realtor who is familiar with the area(s) you’re looking to purchase a home in. They should have “Comps and Analysis” of homes in your price range and with similar amenities that have sold recently in the area. An Agent/Broker may be working with multiple clients at a time, but that is no excuse for poor customer service. That person is working for you and you deserve nothing less than the best buying experience. Never allow an agent pressure you to make an offer on a home you’re uncertain about it. When you find the “right home,” you’ll know. Trust me on this one.

- MAKE SURE YOUR HOME IS PROPERLY INSURED: The worst thing that can happen if a catastrophic event occurs (God forbid) is that the homeowner is “underinsured.” Always check with your insurance provider to make sure you are properly insured. Start with the company that insures your vehicles. Insurance companies such as State Farm, Allstate, Nationwide, Farmers, etc. will usually provide a discount for allowing them the privilege to get that additional commission (cough cough,) I mean insuring your property as well. Shop around to make sure you’re getting the best rate. It’s also a good idea each year to make an appointment with your insurance agent to review your policy and make any changes if necessary.

Although this posting was quite lengthy, the information given should get you started on your quest to a successful home buying experience. CONGRATULATIONS…YOU ARE ON YOUR WAY!!!!

Please feel free to leave any and all comments below. If you have a specific question, email me at Andrea.Coleman@TheFinancialHack.com.

~The Financial Hack ©2015