CHECK OUT THE REPLAY OF LAST NIGHT’S “SCOPING AFTER DARK”

Look for new “Scopes” where I’ll be dropping plenty of “F” bombs… We’re talking FINANCES that is, EVERY MONDAY NIGHT AT 8:30pm CST. Join us.

CHECK OUT THE REPLAY OF LAST NIGHT’S “SCOPING AFTER DARK”

Look for new “Scopes” where I’ll be dropping plenty of “F” bombs… We’re talking FINANCES that is, EVERY MONDAY NIGHT AT 8:30pm CST. Join us.

ATTENTION SCOPERS!!!! Next “LIVE” PERISCOPE BROADCAST Saturday, November 28th from 1-2pm CST. I’ll be starting GoalDiggers Boot Camp 101: DISCIPLINE IS KEY.

I’ll also be finishing up questions I didn’t answer last week regarding CREDIT. JOIN ME as we “Whip Your Finances Into Shape!”

Email your questions to me at AndreaColeman@TheFinancialHack.com

SEE YOU THERE!!!

Credit score this, FICO score that. Blah Blah Blah. Our ability on whether credit is extended to us (or not) can hinge on our FICO/Credit score. What is a Credit/FICO Score? Why is it so important? Some of you may be reading this and thinking, “I already understand credit, it’s importance and how it works.” If you are that person, that’s great. This post isn’t for you. This posting is for the person who doesn’t know what a FICO score is, doesn’t quite understand the importance of the FICO/Credit score, how to mange credit responsibly and how it can impact variables such as interest rates on loans (home, car etc.,) whether additional credit will be extended to you, whether a deposit is required for certain utilities, whether you’re in contention for a job offer, and even car insurance rates. How is it that an insurance underwriter is able to assume because someone’s credit score is fair/poor they are prone to being involved in more car accidents or more susceptible to irresponsible/reckless driving? The same holds true for a potential employer who dismisses an applicant because their credit score is “less than stellar.” Is the employer taking into consideration WHY a person’s credit score is what they deem to be “less than stellar” when making the selection process even though the applicant is qualified for the job? These are serious questions that require serious answers, but let’s not get ahead of ourselves. Let’s first understand what a FICO/Credit Score is.

FICO score and Credit score are usually used interchangeably. Most people call it your “Credit Score” but allow me to give you a bit of background on what the term FICO stands for and what it consists of.

FICO was founded in 1956 as “Fair, Isaac and Company” hence the name FICO by engineer William Fair and mathematician Earl Isaac. The two met while working at the Stanford Research Institute in Menlo Park, CA. Selling its first credit scoring system two years after the company’s creation, FICO pitched its system to fifty American lenders.

FICO went public in 1986 and is traded on the New York Stock Exchange. The company debuted its first general-purpose FICO score in 1989. Scores are based on credit reporting and range from 300 to 850. (Historical information taken from Wikipedia.)

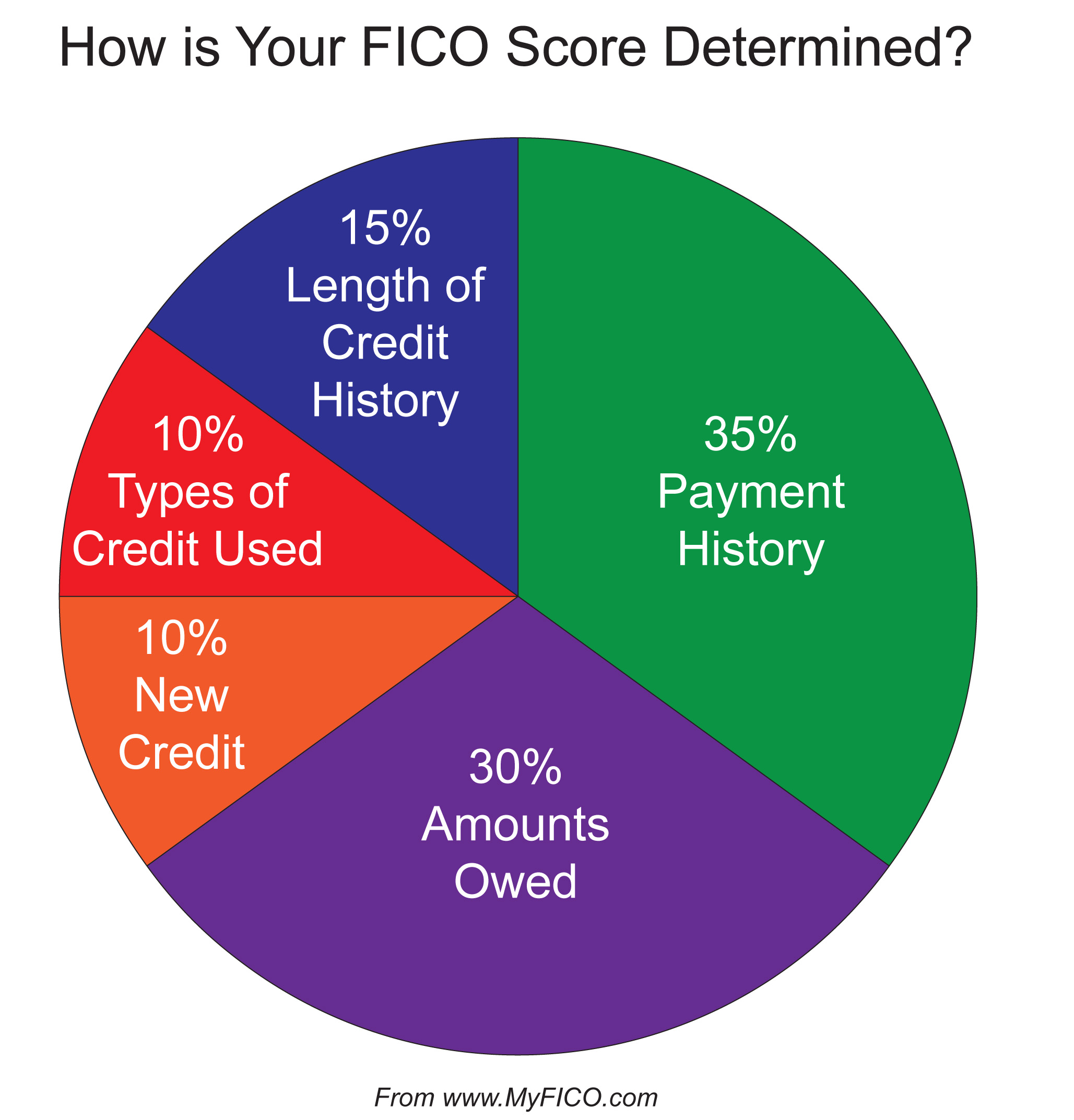

Lenders use FICO scores to gauge a potential borrower’s creditworthiness. Scores are provided by the three credit bureau reporting agencies, Experian, Equifax and TransUnion. There are FIVE components that make up a person’s FICO/Credit score.