When offered 0% financing for a specified number of months, finance charges have already been added to your purchase total. #Fact

Category Archives: Personal Finance

AMERICA SAVES WEEK

In support of America Saves Week, head on over to my Facebook Commmunity Page (The Financial Hack) and post a pic of why you’re saving. It doesn’t have to be fancy. Just a piece of paper will do.

Here’s mine:

Be sure to “LIKE” the community page to leave comments, ask questions, post pictures and participate in future discussions.

Visit http://www.americasavesweek.org for more information.

~The Financial Hack ©2015

MASTERING MULTIPLE STREAMS OF INCOME

Creating multiple streams of income without wearing yourself out can be quite tricky, especially if obligations such as family, school or even your nine to five job take priority. The goal is to find what is easy and convenient… FOR YOU. Here are a few examples of Multiple Streams of Income that I recommend.

- Open an eBay Store: Unlike your classic brick and mortar places of business, your eBay store is a virtual brick and mortar store (minus the overhead.) Just think. There are no costs for leasing space. No utilities. No hassle of hiring employees or having set operating hours. An eBay store allows you the luxury of making money on your own time and on your own terms. If you’re looking for inventory, start by shopping your closet. In my 13 years experience with eBay, I find that new/gently used shoes/handbags/accessories and perfumes are quite popular. Certain books and children’s clothing are popular as well. You can choose to auction your items or sell them outright at a set price (Buy It Now.) Here’s the catch: If you wish to be successful at your eBay store, you must keep inventory in stock at all times (even if it’s just a few items) and a variety of items is preferred. Be mindful of the pricing of your items. Your item is only worth what someone is willing to pay for it.

- Find something you enjoy doing, or are good at… AND FIND A WAY TO MAKE MONEY DOING IT: Are you bilingual? Offer private lessons, or consider teaching an ESL class. Good in Math? Consider becoming a Math Tutor. Are you a “techie?” You’d be surprised how many people would rather NOT install Windows on their computer or do the simplest of troubleshooting when it comes to their computers. That’s where you come in. Do you enjoy exercising, working out and eating healthy? Consider becoming a Personal Trainer. Can you play the guitar, piano or other instrument? Same applies. Do you love animals? Consider dog sitting or becoming a dog walker. Babysitting is very popular among teenaged/college females. Signing with an agency would guarantee you hours and if you’re good at it, word of mouth is the best referral. Catch my drift? These are just a few examples of skills you can tap into to make extra money.

- Write a Book: Years ago before the age of the Kindle and e-books, self-publishing was the most cost efficient way to get your book to the masses. Now, all you need is the manuscript, a good editor (or editing software) and VOILA! Your book is available as a Kindle e-book for $5.99. That isn’t so bad if you’ve sold 2000 units and counting! NOTE: Freelance writing isn’t off limits either. It may take a while to find one, but there are some publications who will PAY for your article submissions so keep your writing skills sharp.

- Become a Substitute Teacher or a Realtor : If your schedule allows, become a substitute teacher. Subbing one day a week could generate an additional $200-$300 monthly depending on whether you hold a college degree or are certified by the state to teach. Also, with the housing market bouncing-back, real estate can be an effective income producer. I’m a licensed Real Estate Broker and it’s always good to have my license to fall back on if necessary. NOW IF ALL ELSE FAILS…..

- Get a Part-Time Job: As much as I hated working part-time jobs in my life, I did it any way because I had to. In high school I worked for a popular fast food chain, in college I worked at a gas station (not as a mechanic lol,) I’ve worked for a grocery chain, I’ve worked making copies at night for a law firm (through a temp agency) you name it, I’ve probably done it. I can recall working a nine to five, driving home, grabbing a quick bite to eat, then heading to my six to ten (or six to later depending on where I was working.) Retail is ALWAYS available, video stores were once popular (until Redbox and Netflix dominated,) and let’s not forget fast food restaurants. For many, fast food is the absolute last resort, but if there were nothing else and you really needed the income, you’d take it. If you just can’t fathom working in fast food, consider Starbucks which offers its employees (even its part time employees) health insurance. There are many people working there just for the health benefits.

So as you can see, there are many ways to generate multiple streams of income. It all depends on your area of expertise as well as your flexibility. Don’t rely on just one stream of income, if possible, have SEVERAL STREAMS because they all have one common denominator; Getting you one step closer to reaching your financial goals. GOAL AFTER IT!!! They aren’t called “Multiple Streams of Income” for nothing.

~The Financial Hack (copyright 2015)

FINANCIAL FITNESS BOOTCAMP WEEK 9: MAMA SAID KNOCK YOU OUT… CREDIT CARD DEBT, THAT IS

As we gear up for the Labor Day weekend, let me finish Part 2 of “Charge Now, Pay Later: Overcoming Debt.” As I stated last week, I know everyone may not have the option to withdraw/borrow from retirement plans or even borrow against the equity in their homes, but never fear….

WEEK 9: MAMA SAID KNOCK YOU OUT…. CREDIT CARD DEBT, THAT IS.

People that know me know not only am I a huge football fan, but a huge fan of boxing as well so what better way to illustrate getting rid of credit card debt than with a boxing analogy. At face value boxing looks like a no-brainer (no pun intended.) One would think the goal is to knock your opponent out as early as possible. Pretty cut and dried right? Not quite. Boxing requires skill and it requires quick thinking. The old “bob and weave” routine may not always work if your opponent is good at anticipating your moves. A boxer’s opponent is watching his eyes, he’s paying attention to his boxing stance. One boxer may have an orthodox stance, another may have a southpaw stance and still another may be able to switch up between the two. Unless you outsmart and/or outbox your opponent, you may end up being the one down for the count. The same applies to “the bout” you’re about to have with credit card debt. And credit card debt WILL NOT be your sparring partner. This isn’t practice, this is the “Real Deal” Holyfield (if you know a little bit about boxing, you understand the lingo.) If not, look it up. There’s nothing wrong with learning new information. You can still overcome credit card debt but once again, this will take some sacrifice on your part and you may be in for a real fight. Don’t underestimate knocking out credit card debt the way some boxers may underestimate their opponent because they’ve been labeled the underdog. Underdogs have been known to upset champions. We see it all the time. Not just in the game of sports, but in the game of life.

By now you should have long tracked your spending and found ways to cut costs. Here are links to a couple of prior posts you may want to reference.

WEEK 2: KNOW WHERE YOUR MONEY IS GOING: https://wordpress.com/post/96150968/19/

WEEK 3: IT’S TIME TO TRIM THE FAT: https://wordpress.com/post/96150968/22/

The extra money you found can be used to pay off credit card debt. Here’s the best “ONE, TWO PUNCH” I recommend for “knocking out” credit card debt:

- Start with the credit card that has the LOWEST balance. Others may suggest starting with the card that has the highest finance charge rate however, paying off the card with the lowest balance FIRST gives you a sense of accomplishment when you make that final payment.

- Use the “Domino Effect” to pay off the next card and so on and so forth. The “Domino Effect” is simply taking the monthly amount used to pay off the FIRST credit card balance and apply it to the amount being paid on the SECOND credit card, the THIRD and… hopefully you don’t have more than three major credit cards. The goal is to pay larger monthly amounts with each card until you have paid them all IN FULL.

Depending on your credit card balances, the process can take a few months or a few years. Think of boxing. Some fights end within the first few rounds, while others go the 12-round distance. How aggressively you attack your credit card debt, as a boxer attacks his opponent, is strictly up to you. Once your credit card balance is paid in full, you can move to other areas of debt such as student loans, car loans and even mortgages (if applicable.) The satisfaction of saying “I have no credit card debt,” is one of the best feelings in the world, especially if that debt was causing unnecessary stress and anxiety. You did it, you stayed the course. VICTORY OVER CREDIT CARD DEBT BELONGS TO YOU!

So there you have it. A simple one, two step plan to overcome credit card debt. I know. It’s easier said than done, but the moment you become sick and tired of being sick and tired, is the moment you take action. The question you must ask of yourself is “Am I sick and tired of being sick and tired?” When you are, you won’t have to ask the question. You’ll already know.

I hope you benefitted from this posting and as always, I greatly appreciate you reading it. Feel free to SHARE. Your commentary is always important so ALL FEEDBACK IS WELCOMED. If there is a specific topic you’d like me to talk about regarding “Financial Fitness Boot Camp” on this blog, feel free to shoot me an email at Andrea.Coleman@TheFinancialHack.com. Don’t miss a posting so be sure to follow me at http://www.thefinancialhack.com.

FOLLOW THIS BLOG AND/OR JOIN THE EMAIL LIST SO YOU DON’T MISS A POST.

HAPPY LABOR DAY!

~The Financial Hack ©2015

FINANCIAL FITNESS BOOT CAMP: WEEK 8 CHARGE NOW…. PAY LATER: HOW I OVERCAME CREDIT CARD DEBT

A couple of you may have been looking for and wondering why there was no posting last week. Simply put, I allowed distractions to get me off task. My lack of focus made it impossible to blog. It wasn’t because I was tired or didn’t have anything to say. I allowed “outside noise” to drown out my internal thoughts. Thank God I’m back on track. Hopefully the “Daily Motivation” postings encouraged you and kept you focused in the interim. Each day is a work in progress for me because there is always a personal/spiritual/professional/financial goal I’m striving to reach. Currently, I’ve set a goal to save a SPECIFIC amount of money over the course of this next year. As a constant reminder of my goal, I’ve written that amount on a piece of paper, taped it to my bathroom mirror and each time the amount increases (i.e. a deposit is made,) I record the date and the adjusted amount. Recording the date helps me track possible patterns in saving.

But it wasn’t always this way. At one point in my life, I wasn’t able to save because (in the words of my younger cousin Bobby,) “I made just enough money to “stay broke.”” That’s certainly what it felt like. This didn’t mean I didn’t make enough money to fulfill my obligations. I simply wasn’t financially mature enough to modify my spending habits. I was still shopping, going on trips (and everything else under the sun) and using credit card(s) when I didn’t have the money. The bills were paid on time every month but without an emergency fund or some type of savings in place, ONE monthly setback could set me back THREE months. For example. What happened if my car was in need of repair? Where would the money come from? My quick fix? I simply incorporated the “Rob Peter To Pay Paul Principle.” I’m sure you guys have heard of it. If you’re honest with yourself, some of you have done it. And if you’re brutally honest with yourself, you’re doing it now. The “Rob Peter To Pay Paul Principle” is sacrificing paying one bill and/or bills to take care of another. This principle worked a few months for me, but eventually imploded in my face.

Let me explain further….

STEP 8: CHARGE NOW…. PAY LATER: HOW I OVERCAME CREDIT CARD DEBT

I was never taught how to use credit responsibly. By the time I entered college, the only advice given to me regarding credit (credit cards in particular) was, “DON’T GET ‘EM!!! DON”T USE EM!!!” That came from both my mother and father. They were the traditional “old school” types who believed in cash and carry. But how could a broke freshman pass up the opportunity to get a free college t-shirt just for “signing up?” Before I knew it, I had THREE FREE T-SHIRTS and was issued TWO CREDIT CARDS with a credit limit of $500 each. Now how did this credit thing work again?

I was responsible with the charges I made but not responsible with how I made the payments. I thought I could make payments at my discretion as long as the balance didn’t exceed the credit limit. That’s the way credit cards work. Right?

One day (at the mall of course,) a purchase for a pair of shoes was declined. I gave the salesperson my other card. Declined as well. I didn’t understand why. I hadn’t gone over my limit, so why were the cards being declined? The salesperson suggested I contact the credit card company. After sifting through unopened mail, I found a statement and proceeded to contact them. Not only had I not paid in three months, but my balance exceeded the credit limit. What? How could this be? APR? Finance charges? What is that? Late fees? For what? The Customer Service Representative I spoke to was kind enough to explain the abbreviated version of Credit Card Management For Dummies to me. (Hmmm. I like that. I’ll file that in my mental mailbox and blog about Credit Card Management for Dummies in a future post.) Long story short, Mom to the rescue. She paid the balances on the cards provided I close the accounts. Those were her terms and in my case, the one with the money calls the shots. Fast forward to my ADULT adult years. I’m well out of college with two degrees, still couldn’t manage my credit card debt and in my late 30s. By this time, I had knowledge of credit cards and how they worked, making timely payments etc., but the temptation to spend spend spend when one bank is offering you a $15K line of credit and another a $10K line of credit was too great. There’s a little way banks can really “stick it to you” if you’re not careful. I’ll give you two words: CASH ADVANCE (which yield HIGHER interest rates than making regular purchases.) When I was going through my “Keep Up With The Joneses” phase, where I had to have the Mercedes Benz, the larger home, and designer handbags to feel validated, those 3-4 little checks the bank would send with my monthly statements came right on time. The next thing I knew, the balance on one credit card was near maxed out, and I was working on maxing out the second card. What to do? Back then, the minimum payment on the TWO credit cards combined at the time totaled half of the mortgage on my home. Plus I also had a car payment on my truck. There was no way I was going to ask my parents. I made my bed, now it was time to lie in it. I had credit card debt in excess of $20K. My credit was shot as my debt to income ratio was so high, there was no way a creditor/lender would extend another dime of credit to me for anything. There was the constant anxiety and worry. Anger and irritability. Sleepless nights. Dreams of falling then waking up in cold sweats. Worry that I’d have to sell my investment properties, face foreclosure and file for bankruptcy. Thinking of it as I type now makes me anxious. That’s a place I never want to visit again.

YEAH YEAH YEAH. WE GET IT. YOU WERE DROWNING IN CREDIT CARD DEBT. SO HOW DID YOU OVERCOME IT? I know this is what you guys want to know. I had to set the scene in order to illustrate how the CHARGE NOW….PAY LATER way of thinking caught up to me.

Here’s how I did it: I “settled” with the two credit card companies.

“Settling” with a credit card company means you agree to pay the credit card company (i.e. bank) an amount LESS than the current balance on your credit card. The bank will in turn close the account and send you a 1099 (which you MUST declare as income during the tax filing year.) The banks will usually try to work with you on a settlement amount. For them, It’s better to get SOME of the money back, than no money at all. Here was my settlement break down:

Credit Card 1: Balance $15,000 (apprx) Settlement Amount: $7,500.

Credit Card 2: Balance $8,000 (apprx) Settlement Amount: $3,000.

The bank refused to accept any thing less than half the balance on Credit Card #1. For Credit Card #2 I told the bank $3000 was all I had to settle with. They accepted what I offered.

IF YOU SETTLED FOR APPROXIMATELY $10K AND PREVIOUSLY STATED YOU HAD NO SAVINGS, HOW WERE YOU ABLE TO PAY? Answer: I was forced to tap into my IRA and take the hit (penalty) for a partial withdrawal. Some of you may have been in the workforce long enough to have a retirement account saved up. If so, you can take a partial withdrawal from your retirement account (if allowable) or take out a loan against it, which of course will have to be repaid. It may not sound attractive, but it’ll get the “monkey” off your back. The downside. My credit score would suffer, but who cares! It was beyond insufferable anyway. But wait. there was a silver lining to this credit card debacle. A THIRD credit card which I rarely used. Let’s just call it a “rainy day” card. It had a pretty sizeable credit limit like the others so if push came to shove, it was there to use. Or so I thought. That lone credit card that once had a limit in upwards of $10K had been reduced to $2000. Couple that with my POOR credit rating at the time, and that was just the motivation I needed to become more responsible when it came to my finances. I was sick and tired of being sick and tired.

My father’s ever so redundant line when it comes to credit cards, “If you have to use a credit card to buy it, you can’t afford it,” still resonates with me today. That may make sense to him, but I would tweak that line just a bit. “If you can’t pay your credit card balance in full when you get the bill, you MAY NOT be able to afford it.” I like my wording better. Less harsh and more accurate. Everyone’s “financial collage” is different and no two collages will ever look exactly the same. Today I still have the one credit card and although the bank has been gracious to increase its limit (enticing me to use it no doubt,) the only action it gets is the random fill up at the gas station and the occasional dinner with me of course paying the balance in full at the end of the month.

This happened at age 40. I am now 44. And I’ve come a LONG WAY in four years. It only took about a year and a half of strictly managing my finances responsibly to INCREASE my credit score rating from POOR to GOOD. And you can do it too. Even if you don’t have a retirement account, you can still eliminate credit card debt. Look for tips in next weeks blog posting.

I hope you benefitted from this posting and I do appreciate you reading it.Your commentary is always important so ALL FEEDBACK IS WELCOMED. If there is a specific topic you’d like me to talk about regarding “Financial Fitness Boot Camp” on this blog, feel free to shoot me an email at Andrea.Coleman@TheFinancialHack.com. Don’t miss a posting so be sure to follow me at http://www.thefinancialhack.com.

FOLLOW THIS BLOG AND JOIN THE EMAIL LIST SO YOU DON’T MISS A POST.

~The Financial Hack ©2015

FINANCIAL FITNESS BOOT CAMP: WEEK 7

If you read my blog post from Week 5: “You’ve Got To Be in Position To Make The Completion,” you know I love football. And if you’re a fan as well, you know football season is drawing near. Of course there are players (rookies) that were drafted by the team and there are other players that “tried out” for the team, but have to “prove themselves” if they wish to stay. After observing a few players in practice as well as their performance in scrimmage and Pre-Season games, the coaching staff has to make decisions regarding the upcoming player roster: Who Stays vs. Who Goes. So many factors can determine a player’s fate: performance on the field (and sometimes off,) depth of the team, injury (or injury history), age, and many other factors. This is always a stressful time for players and the coaching staff as decisions whether a player stays or goes in some cases takes careful consideration. Some coaches know right away who is an “asset” to the team and who is a “liability.” For all practical purposes, let’s use another football analogy regarding your finances as you begin to budget your money by FIRST asking yourself this question……

STEP 7: WHAT HAS TO BE CUT FROM YOUR SPENDING HABITS?

You’ve had plenty of time to track your spending. You’ve trimmed the fat, now it’s time to make some SERIOUS cuts. Some feelings are going to get hurt after the cuts (mostly yours,) but with great sacrifice comes great reward. For your budgeting to be effective, you have to stick to it. DISCIPLINE IS KEY. So as an example, let’s take a look at some areas of my spending that DIDN’T make the cut and for all practical purposes, I’ll use basic football positions you all should know… hopefully.

1st CUT (KICKER): SHOPPING FOR NON-ESSENTIAL ITEMS– In football, a “Kicker” kicks off the ball to the opposing team, kicks the extra point after a touchdown as well as attempt 3pt field goals when scoring a touchdown is not obtainable. As much as I love thrift stores, and discount retailers (TJ MAXX, Marshall’s, Ross, DSW etc.,) these are considered “Kickers” to me. These non-essential items are purchased to score extra points. An outfit here, another pair of shoes there, accessories I don’t need, or makeup I may only use once. The kicker is my bonus, my “extra points” if you will. If you walked inside my closet or looked in my bathroom, you’d understand why. I need not another article of clothing, pair of shoes, or tube of lipstick.

2nd CUT (SAFETY): EXCESSIVE BEAUTY APPOINTMENTS– A “Safety” is a team’s last line of defense because they are furthest from the line of scrimmage. Safetys usually assist Cornerbacks with a deep pass that may be thrown to a Wide Receiver or in some cases, a Tight End. If I’ve lost you completely with football jargon, just nod and pretend you understand. Vanity is a “safety net” for some of us, because in essence it can be the last line of defense for us. Some aren’t comfortable leaving the house unless they’re in full regalia; hair, makeup, nails, etc. hence our “last line of defense” to be noticed or to catch someone’s attention. As a rule of thumb I chose ONE ELEMENT OF VANITY to keep, my “Safety” and that was maintaining my bi-weekly hair appointments. If a sacrifice of vanity has to be made, I’m willing to bet hair will win every time (especially if your hair requires a high level of maintenance.) Some spend monies on eyebrow waxing/threading or whatever the latest technique is. I grab an eyebrow brush, a pair of tweezers, shaping scissors, a razor and go to work. The result looks great. At times, I will “glam it up” and add some “oomf” to them when necessary, but for now, the brows are just fine. I reserve perfecting my brows for special occasions, church, funerals, and weddings only (lol.) There’s also a new trend with eyelash extensions. As great as they look, the maintenance can be quite costly. For me, that’s nothing a good tube of mascara and eyelash booster can’t fix. The same goes for nails. When I was going to the nail salon regularly (over 15 years ago,) acrylics was the “in thing.” Now it’s gel nails. I grab a bottle of Sally Hansen’s “Hard As Nails” and the Essie nail color of my choice and hit up the nail salon for a $10-$15 manicure (which comes from my monthly discretionary income.) The result. Healthy nails. The same goes for Pedi’s. You can actually do your own pedicure at home but I usually have a professional pedi done monthly (again taken from my monthly discretionary income of course.)

3rd CUT (RUNNING BACK): EATING OUT EXCESSIVELY– Now I know even those who despise football know what the function of a “Running Back” is or can at least name one. Running backs receive the ball (usually handed off from the quarterback) and “rush the play.” Running Backs are usually of average height but are very strong and powerful when rushing through a group of linemen. Just as a Running Back rushes through a group of lineman, for some (like me,) it is so easy to make a “rushing play” to grab some fast food or a bite to eat at a restaurant/bistro to keep from having to cook. I was more responsible when I was married, but as a single adult, it’s just so much easier to pick something up on the way home. I keep referring to the $500 I spent eating out in one month. This included stops for breakfast on the way to work, lunch, and dinners/brunch out with friends. $250 can get me a refrigerator and pantry full of food. Prepackaged dinners always come in handy, and I’m not above eating Ramen Noodles (shrimp flavor is my favorite.) Eating Ramen noodles has nothing to do with being poor and not being able to afford anything else, hell, I like ’em, they’re economical, and it doesn’t take long to prepare them. As convenient as it is to hit the nearest Luby’s drive thru for Chicken Fried Steak, mashed potatoes, cabbage and a wheat roll, the $11 I spend on that ONE MEAL can get me all the items I need to make a spaghetti or enchilada dinner that I can stretch an ENTIRE WEEK. Also consider items such as salads and baked potatoes. Carnivores feel free to add some grilled chicken to that salad to make it interesting. And NEVER sleep on Hamburger Helper. They have so many different flavors now, it’s ridiculous. Again. Sacrifice is required in order to reach your goal. You may be eating Hamburger Helper now, but you’ll be eating steak and potatoes in little or no time if you stay the course…. YOU CAN DO THIS!!!

SO HAVE YOU DECIDED WHAT NEEDS TO BE CUT FROM YOUR BUDGET? Hopefully the examples I mentioned will give you an idea on where you can make some cuts. You’ve got some tough decisions to make if you haven’t. If you want to be financially free, you’ve got to be willing to let some things go. I’m sure a few of you have already put those players aka “spending habits” on the “chopping block” that pose more of a liability than an asset to your finances. Good for you. To those that still haven’t decided, MAY “THE FORCE” BE WITH YOU. I KNOW YOU’LL MAKE THE RIGHT DECISION. HAPPY CHOPPING!!!!

I hope you benefitted from this posting and I do appreciate you reading it. I want to hear from you! What is posing a “liability” to your finances and what have you decided to get rid of? Your commentary is always important so ALL FEEDBACK IS WELCOMED. If there is a specific topic you’d like me to discuss regarding “Financial Fitness Boot Camp” on this blog, feel free to shoot me an email at Andrea.Coleman@TheFinancialHack.com. Don’t miss a posting so be sure to follow me at http://www.thefinancialhack.com.

FOLLOW THIS BLOG AND JOIN THE EMAIL LIST SO YOU DON’T MISS A POST.

~The Financial Hack ©2015

FINANCIAL FITNESS BOOT CAMP: WEEK 6

By now, you’ve had time to track your spending for ONE month and have identified patterns and trends in your spending habits. Are you spending too much money shopping for items you don’t need? What about dining out (like myself?) Going overboard on leisure activities and vacations? What about overindulging your children? Yourself? The list can go on and on. You know where your money is going because you’ve tracked it. If you’re serious about eliminating debt, you know EXACTLY what you need to do to get there. This post won’t be as lengthy as the others because you need time over this next week to THINK and DECIDE if you’re ready…

STEP 6: IT’S TIME TO GET OFF THE MERRY GO ROUND… OF DEBT

A MERRY-GO-ROUND is defined as:

1. A revolving machine with model horses or other animals on which people ride for amusement.

2. A large revolving device in a playground, for children to ride on.

BUT FOR THOSE WHO WANT TO BECOME “FINANCIALLY FIT” THE MERRY-GO-ROUND OF DEBT IS…..

3. A continuous cycle of activities or events, especially when perceived as having no purpose or producing no result.

For some of us, debt is similar to a merry-go-round, especially when we take no steps to eliminate it. Doing so, is a continuous cycle, having no purpose and produces no result. For example, the minimum amount you pay each month on your credit

card(s) DOES NOT get you any closer to paying off the credit card balance in a reasonable period of time. Credit card statements now show how long it would take to pay off a credit card balance making minimum payments (and of course making no future charges.) Have you stopped to read it? For some it may take up to 30 years to pay a balance. THIRTY YEARS!!! What if you’re only 30 years old? Oh, Perish the thought. “But I pay on time and I have good credit,” is what some of you may be thinking. Paying the minimum amount due on time shows you are responsible at handling credit, but your debt-to-income ratio can still be through the roof labeling you a possible “credit risk.” Although creditors see you making timely payments each month, they may be hesitant to extend additional credit to you, or in some cases may charge you higher interest rates, or require higher down payments to do so.

Debt, or credit card debt in general is a vicious cycle that some of us see no end to. Many have the belief that debt is a part of life. SAYS WHO? Eliminating credit card debt is the first thing I’d like to tackle, but BEFORE we start tackling credit card debt, it would be wise to set up an emergency savings account. To do so, you have to be willing to “get off the merry go round.” GIVE THOSE CREDIT CARDS UP!!!! Remove them ALL from your wallet or pocketbook and only carry one (with the lowest credit limit) in case of emergencies ONLY.

Now how does “Getting Off the Merry-Go-Round” relate to the tracking of my spending habits and credit card debt?

YOU’VE GOT TO EXERCISE DISCIPLINE AND BE WILLING TO LET SOME THINGS GO. This means scaling back on the spending of non-essential items. Look at your what you’ve spent your money on in the past month and determine what can be modified or stricken completely from your spending in order to free up additional money so you can pay not only the minimum amount due on your credit cards, but a “little extra.” I’ll talk more about how I tackled credit card debt (in excess of $20K) in next week’s FINANCIAL FITNESS BOOT CAMP post… AND IT AINT PRETTY!!! In the meantime, let’s start working on how to build up that EMERGENCY FUND. Look for PART 2 of this post later this week.

Old habits die hard, but the reward from discipline far outweighs the cost to reach your goal. So are you IN or OUT? Will you remain shackled by debt, or break the chains to gain financial freedom? The decision is up to you.

I hope you benefitted from this posting and I do appreciate you reading it.Your commentary is always important so ALL FEEDBACK IS WELCOMED. If there is a specific topic you’d like me to talk about regarding “Financial Fitness Boot Camp” on this blog, feel free to shoot me an email at Andrea.Coleman@TheFinancialHack.com. Don’t miss a posting so be sure to follow me at http://www.thefinancialhack.com.

FOLLOW THIS BLOG AND JOIN THE EMAIL LIST SO YOU DON’T MISS A POST.

~The Financial Hack ©2015

FINANCIAL FITNESS BOOTCAMP: WEEK 5

STEP 5: YOU’VE GOT TO BE IN POSITION TO MAKE THE COMPLETION.

This should be the last week of you tracking your spending habits for the month. It’s do or die now. Once you have tracked your spending, you can get a better handle on where your money is going. Remember the month I tracked my spending, $500+ dollars was wasted on “eating out.” Once this week ends, do the math and see where the bulk of your money is going. If you see that a considerable amount is being spent on non-essential items, it’s time to ‘get into position to make the completion.” Let me explain what I mean.

I’m a HUGE Dallas Cowboys fan. I’m a huge football fan in general, but for all practical purposes, I’ll use my favorite

team and favorite Dallas Cowboy Wide Receiver Dez Bryant for this illustration:

Before I continue, Yes, this photo is OLD. 2009 to be exact. Yes, I drag this photo out and post it on social media at the start of EVERY SINGLE FOOTBALL SEASON. This picture was taken around the time Dez had just signed with the Cowboys as a rookie and was temporarily living in the same suburb as myself. I met him at a local restaurant. He was walking around with a small entourage and everyone was whispering “That’s Dez Bryant.” I recognized him, stopped him and asked if he wouldn’t mind taking a photo. He was real cool about it. I thanked him and he said “Yes Ma’am.” MA’AM? Now hold on! I don’t look THAT old, not then and certainly not now. Anywhoo, that was six years ago and let me tell you. Dez doesn’t look anything like he does in this photo anymore. Let’s just say milk DOES DO the body good… and as always, I DIGRESS. Hold on while I fan myself. Whew!!! Okay. Back to illustrating my point.

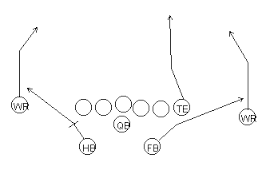

When Dallas Cowboy QB Tony Romo calls a slant route where Dez is the intended receiver, Dez has to be in the RIGHT PLACE at the RIGHT TIME otherwise, he won’t be in position to catch/receive the ball. Here’s what a version of a slant route play looks like to the football enthusiast:

A slant is where a receiver runs straight then hits a 45 degree angle behind defensive linemen to receive a pass. Romo can throw a perfect pass but if Dez isn’t there to receive it, the Cowboys have lost a down or in Romo’s case, there’s a strong possibility he’s thrown an interception. Now let me tie this in to how this relates to YOU:

Financial independence requires DISCIPLINE. Financial independence requires PATIENCE and financial independence involves FOLLOW-THROUGH. These are the same techniques Dez uses on the field that allow him to make “the big plays.” If you want to make the “big plays” and achieve financial independence you must first be DISCIPLINED. That means you may have to sacrifice some things in order to complete the play. You will also have to incorporate PATIENCE into your thought

process. Financial independence doesn’t happen overnight (unless you win the lottery,) and even in some cases, the winners still manage to blow ALL their winnings leaving nothing to show. To make the “big plays” and reach your goal of financial independence, you must FOLLOW-THROUGH. You can’t give up on your goal. If Dez is running too fast, the pass may be thrown behind him, too slow and it may thrown in front of him, but if the timing is just right, he makes

the play, gains some yardage and may even score a touchdown. You don’t need the touchdown just yet. Right now, your goal is to complete passes and continue to gain yardage. Then you’ll complete more passes. And gain even more yardage. Keep completing passes, keep completing tasks, and YOU WILL score the touchdown!

I am so excited for those of you that have actually taken on the task to take charge of your finances by tracking your spending habits and even those who may have just decided to begin this process. It’s never too late to get on board. Touchdowns can happen at anytime during a football game. The same applies to the commitment you’ve made to yourself. The commitment to pull yourself out of debt, the commitment of becoming a better steward of your money, the commitment to make better decisions regarding your finances. The “end zone” awaits.

Consider this posting the “Pep Talk” you get before the “big game.” For those that intend to get in the game, make sure you bring your “A” game. Leave the B, C, D and certainly your “F” game at home.

I hope you benefitted from this posting and I do appreciate you reading it.Your commentary is always important so ALL FEEDBACK IS WELCOMED. If there is a specific topic you’d like me to talk about regarding “Financial Fitness Boot Camp” on this blog, feel free to shoot me an email at Andrea.Coleman@TheFinancialHack.com. Don’t miss a posting so be sure to follow me at http://www.thefinancialhack.com.

FOLLOW THIS BLOG AND JOIN THE EMAIL LIST SO YOU DON’T MISS A POST.

~The Financial Hack ©2015

FINANCIAL FITNESS BOOT CAMP WEEK 4

(Previously posted via Tumblr July 22, 2015)

STEP 4 : FINANCIAL HACKS

While those who still have 2 ½ weeks left to track their spending for the month, I thought I would share some financial hacks I use to keep me on track with my spending.

1. PAY GOD FIRST: As not to offend anyone, I say pay God FIRST (if applicable.) Not everyone believes in paying tithes or haven’t been taught to trust God with their first fruits, so again I say: PAY GOD FIRST (if applicable.) If this applies to you, you may choose to pay tithes based on your pay schedule. Some people pay tithes monthly as if they would pay their rent or mortgage, others bi-weekly or bi-monthly. Whatever method works for you, give Him what belongs to him FIRST. I guarantee the giving of your first fruits will help you to become a better steward of your money.

2. GIVE YOURSELF A MONTHLY ALLOWANCE: Depending on how much discretionary income you have to work with after determining how/where your money is being spent, give yourself a REALISTIC monthly allowance. It can be weekly or monthly. I prefer a monthly allowance. I withdraw the allowance I’ve set for myself from the ATM at the beginning of each month. Using reloadable Debit Cards work just the same. If that amount is spent BEFORE the end of the month, I’m SOL and have to wait until next month’s allowance. Anything I don’t spend is placed into a savings account. Keep in mind monthly allowances can cover items such as eating out, entertainment, manicures, pedicures, and non-essential items such as clothing, makeup, etc.

One of the things that works for me is using my reloadable Starbucks card. I allow myself $25 each month for my Grande (Venti depending on how late I stayed up the night before) Caramel Macchiato.

I usually save these as a treat and will stop on my way to work Saturday mornings. I always make sure to get a receipt so I know how much is left. NOTE: I NEVER HAVE A CARRYOVER BALANCE. This is a good system for me because at one time I was making Starbucks trips 3-4 times/week and that can add up. Remember…. Financial Fitness requires discipline (there’s that word again.)

3. KEEP YOUR OWN CHANGE: Although banks have the “Keep the change program,” I’ve been keeping my own change. If I grab a couple of breakfast items from the dollar menu at McDonalds, I use my allowance to pay for it. It’s a non-essential item because I could have easily scrambled an egg and made some toast before I left for work. If the cashier asks me in the drive thru if I have two pennies, I’ll say “No” because I want that .98 in change she’s going to give me back. Once my ashtray fills up, I transfer the change into my Crown Royal bag (don’t act like you don’t have one right now full of pennies) until I’m able to separate the change and put it in separate coffee canisters. Remember, I had $240 (well $238.88) I saved up from last year. We’ll see by July 2016 how much change I’ll have saved since I’m using cash much more than my debit card these days.

4. TAKE THOSE CREDIT CARDS OUT OF YOUR WALLET: Leave that Visa, MasterCard, Discover, AmEx, Diners Club Card etc. AT HOME! You don’t need all those cards in your wallet. It may be too tempting for some of you. If you’re bold enough, you’ll take them ALL OUT. Unless you have a reserve amount in your checking account/overdaft protection savings account that’s tied to your checking account, I don’t advise this. CARRY ONE CARD IN YOUR WALLET/POCKETBOOK FOR EMERGENCIES ONLY. You may not be ready to cut the others up, but if you’re serious about deleting credit card debt, you may want to consider it (but we’ll cover credit/credit cards as the weeks proceed as well.) If you have a gas card, leave it at home unless you’re religious about paying the balance in full at the end of each billing period. If you do pay your balance at the end of each month, that’s great. This can actually be a good system for couples who have gas cards issued from the same account. Paying the balance each month also helps boost your credit score.

Some good advice my Dad gave me regarding credit cards, “If you can’t pay cash for it, then you can’t afford it.” Wise words to live by.

These were just a few financial hacks I could think of off the top of my head. I’m sure others I use will come to mind and I will share them with you as well. As always, I hope you benefitted from this posting and I do appreciate you reading it. Your commentary is also important so ALL FEEDBACK IS WELCOMED. If there is a specific topic you’d like me to talk about regarding “Financial Fitness Boot Camp” on this blog, feel free to shoot me an email at AndreaColeman@TheFinancialHack.com. Don’t miss a posting so be sure to follow me at http://www.thefinancialhack.com.

FOLLOW THIS BLOG AND JOIN THE EMAIL LIST SO YOU DON’T MISS A POST.

~The Financial Hack ©2015

FINANCIAL FITNESS BOOT CAMP: WEEK 3

(Previously posted via Tumblr July 13, 2015)

STEP 3: IT’S TIME TO START TRIMMING THE FAT.

Hopefully you’ve started tracking now where your money is going by documenting EVERYTHING you’re spending your money on and recording HONEST, ACCURATE information. Don’t worry. It’s okay if you bought that pair of shoes you didn’t really need. Record it anyway. I downloaded three old school albums and a few additional songs from iTunes last week… but I documented it. Remember, the point of tracking your spending is to notice patterns/trends in your spending habits. As mentioned in my last blog, after a month of tracking my spending habits, I discovered over $500 was being wasted on “eating out.” YIKES!!! It’s under control now. TRUST ME.

If you have decided to track your spending habits for the month, here’s how you can get a head start on becoming “financially fit.”

IT’S TIME TO START “TRIMMING THE FAT.”

Now you may be thinking, “How can I start trimming the fat if I’m not done tracking my spending habits for the month?”

START WITH YOUR HOUSEHOLD BILLS.

You should already know your monthly mortgage amount unless you have an ARM (Adjustable Rate Mortgage) and if you do, RUN TO YOUR BANK AND REFINANCE QUICK!!! I’ll cover mortgages as the weeks progress. I want to focus on household bills such as electricity, telephone, satellite/cable, and additional household services that can be negotiated. It’s a good practice to sit down and re-evaluate what amounts you’re paying for these services each year. Take your satellite/cable service provider for example. I believe bundle packages (cable, phone and internet) being offered is a great idea, but have you stopped to look at what you’re paying for? Think about it. Do you REALLY have to have the “premium channel package” that includes every movie and sports channel known to man when you only watch a handful of channels that are more than likely offered in the company’s “standard channel package?“ Is it necessary to have “turbo speed” internet connection? Is the information you’re uploading/downloading work-related which would require faster speeds when working from home? These are features that can save you money. I recently switched back to DirecTV and am paying a bill much lower than I was before I left them for Time Warner Cable. Take advantage of satellite/cable company offers. It’s been my experience there’s usually a 12 month commitment which I don’t mind since I don’t plan on going anywhere and if I move I can move the service with me thus, no interruption. By switching back to DirecTV, I am saving approximately $75/month. If you are satisfied with your current provider and do not wish to switch companies, you can always re-negotiate. My favorite line is, “I can’t afford cable anymore, is there anything you guys can do to help me out because I REALLY don’t want to disconnect my service but I may have to.” The satellite/cable providers DO NOT want to lose your business so trust me, they’ll do everything in their power to keep it. Customer Service Reps usually have a lot of leeway and can offer you lower prices on packages and services, BUT YOU WON’T KNOW THEY’RE AVAILABLE UNLESS YOU ASK. The same works with your electricity provider because you can negotiate a lower price per kilowatt hour, for example, lowering your price from 12.4 cents per kilowatt hour to 10.9 cents. It may not seem like a big difference, but every little bit helps. Try it. You’ll be surprised.

NOTE: I prefer to use “average billing” with my electricity provider. This way my bill is the same amount each month. I like to see consistent numbers with my monthly household bills. It’s just a personal preference.

Household services can be negotiated, modified or terminated if necessary. As much as I loved the cleaning service who came every two weeks, I knew if I wanted to save more money, I could no longer keep them. So guess who’s doing the cleaning now? The same person that was doing the cleaning BEFORE someone else started doing it for me. As far as the pool cleaning service I use, I couldn’t let them go however, I’m investing in a pool cover. This way I can save approximately $1200 each year. I should have done this when I first moved in my home, but I just recently started getting REALLY SERIOUS about building up a nice nest egg.

What about your landscaper? I don’t know what you call yours, but I call mine “the yard man.“ At one time, I used to cut my own yard and it looked just like professionals were maintaining it, but that got old pretty quickly. My current landscaper charges me $25 to cut the front and backyard (which is a lot of yard by the way.) But here’s the catch: He’s been my landscaper/yard man for the past 15 years. Bottom Line: Relationships are important. If you have a landscaper you’ve been using for a while, ask to re-negotiate. If you have a great relationship with them, they shouldn’t have a problem coming down on the price.

The household expenses mentioned in this blog were expenses I felt were most basic and necessary to discuss (and were based on my personal re-evaluation/re-negotiation.) Until you get a better picture of your spending habits/trends after the first week of August, you’ll be ready to trim even more fat. It’s gonna get ugly, SO GET READY!!! Let me know how the tracking of your spending habits is coming along. I appreciate the Twitter feedback from @whois_atiya regarding last week’s blog posting. I’m so glad I was able to offer information you found useful. Keep that feedback coming!!!

As always, I hope you benefitted from this posting and I do appreciate you reading it. Your commentary is also important so ALL FEEDBACK IS WELCOMED. If there is a specific topic you’d like me to talk about regarding “Financial Fitness Boot Camp” on this blog, feel free to shoot me an email at Andrea.Coleman@TheFinancialHack.com. Don’t miss a posting so be sure to follow me at http://www.thefinancialhack.com.

FOLLOW THIS BLOG AND JOIN THE EMAIL LIST SO YOU DON’T MISS A POST.

~The Financial Hack ©2015