Join me and “The Goal Patrol” on Periscope as we discuss goal mapping and its benefits. Tune in tonight at 8:30pm (CST) on CACTV (@IAmCoachAndrea)

The Dream Is Real… Hard Work Sold Separately.

~The Financial Hack ©2015

Join me and “The Goal Patrol” on Periscope as we discuss goal mapping and its benefits. Tune in tonight at 8:30pm (CST) on CACTV (@IAmCoachAndrea)

The Dream Is Real… Hard Work Sold Separately.

~The Financial Hack ©2015

CHECK OUT THE REPLAY OF LAST NIGHT’S “SCOPING AFTER DARK”

Look for new “Scopes” where I’ll be dropping plenty of “F” bombs… We’re talking FINANCES that is, EVERY MONDAY NIGHT AT 8:30pm CST. Join us.

TWO NEW “SCOPES” ARE AVAILABLE FOR VIEWING:

FINANCIAL DISCIPLINE IS KEY:

CREATIVE SAVING WITHOUT THE EFFORT:

CHECK EM OUT. THE “REPLAYS” WILL BE GONE BEFORE YOU KNOW IT.

Thanks in advance for watching and for your support.

~The Financial Hack ©2015

Live Broadcast…. COMING SOON!!! You’ve READ my postings on my website, now SEE AND LISTEN to what I have to say via Periscope. Follow me at: The Financial Hack. See you there!!!

It’s not about how much you make, it’s what you do with what you make that counts.

~The Financial Hack

I took a trip to H&M Store this morning. There was a location nearby that opened over the weekend. A 10 minute drive to Uptown Village sounded a whole lot better than a 25 minute drive to the nearest location at Northpark Mall. I heard the prices were reasonable and the clothing was trendy. Ehhh. I’m not really a “trendy” dresser. I opt for more “classic” pieces which I believe compliment my personality. Don’t misunderstand me. I’m not some snot who turns my nose up and frowns upon things that don’t suit me. For those that remember me from my YouTube vlogging days, YOU KNOW ME…. AND THAT AINT ME, but I digress.

I made a pit stop at Starbucks for a Venti upside down Caramel Macchiato with extra whip then headed for the ATM. I gave myself a $100 budget. That was NON-NEGOTIABLE. If my purchases totaled $105.32, something was going back on the rack. Seriously. Unfortunately, I didn’t purchase anything. Or maybe good fortune was on my side. I probably would have had buyer’s remorse before I got to the car. I tweeted earlier this morning although I saw a few attractive items in the store, nothing grabbed me. I refused to make a purchase just because I was there. I did walk around the store twice to make sure I didn’t miss anything. I saw some button down shirts that could have worked for me, but decided against them. Then I saw a couple of blouses that may have worked, but they looked a little flimsy and thin. I’m sure I would have found fault with any and everything that caught my attention. Could it be I wasn’t in the right headspace? Could it be since meeting financial goals is my focus, not to mention I already have a closet FULL of clothes, something didn’t “feel right.” Something was off. I instantly felt the guilt of wasting $100 just to say “Hey! I went to H&M and this is what I purchased.”

One thing I look for in clothing is “quality.” I’ll take quality over quantity any day of the week. To be honest, the higher-priced items were of better quality than the lower-priced items. I saw a couple of dresses in the $50 range that would have worked for me, but in all honesty, I could find the same style of dress at one of my many favorite thrift stores I patronize for half the price and the dress would most certainly have a label in it. See where I’m going with this?

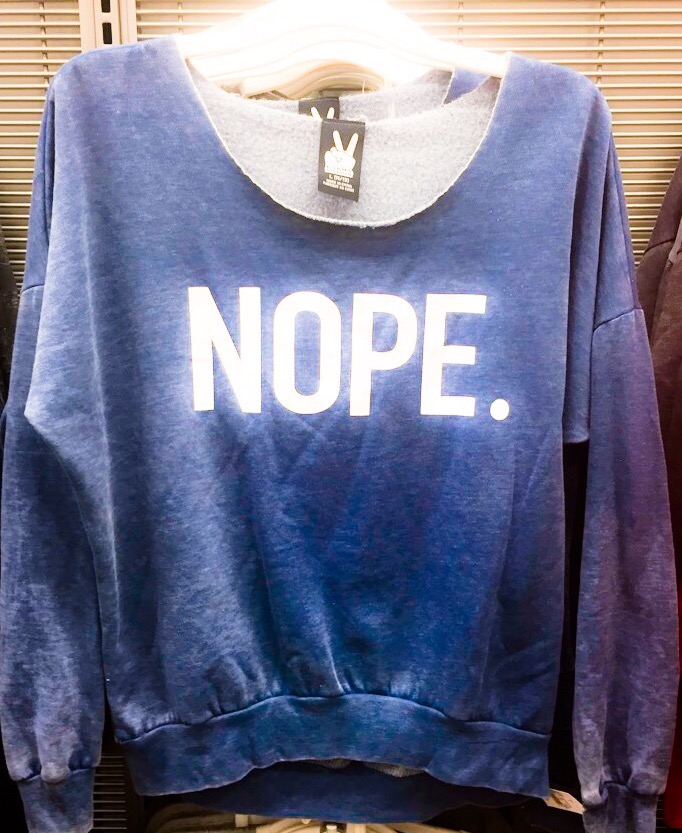

I left the store empty handed and stopped at a nearby Target which carries career clothing in my style and price range. No luck there either. Again, it’s the headspace I’m in. I’m wasn’t in “shopping mode,” I was in “saving mode” and had been there since BEFORE I left home. I’ve got a good system going so why disrupt things now? Honestly, I didn’t want to spend my money on clothing. Was my mission today based on a NEED or a WANT? Well, that’s a “no brainer.” At least it is if you’ve read this far. I WANTED to buy clothing from H&M, I didn’t NEED to. I WANTED to buy clothing at Target, I didn’t NEED to. I did however purchase this sweatshirt:

I purchased it as a reminder of what to say, when I’m about to make an UNNECESSARY PURCHASE:

How befitting…. For me. $21.64 spent just to make a point.

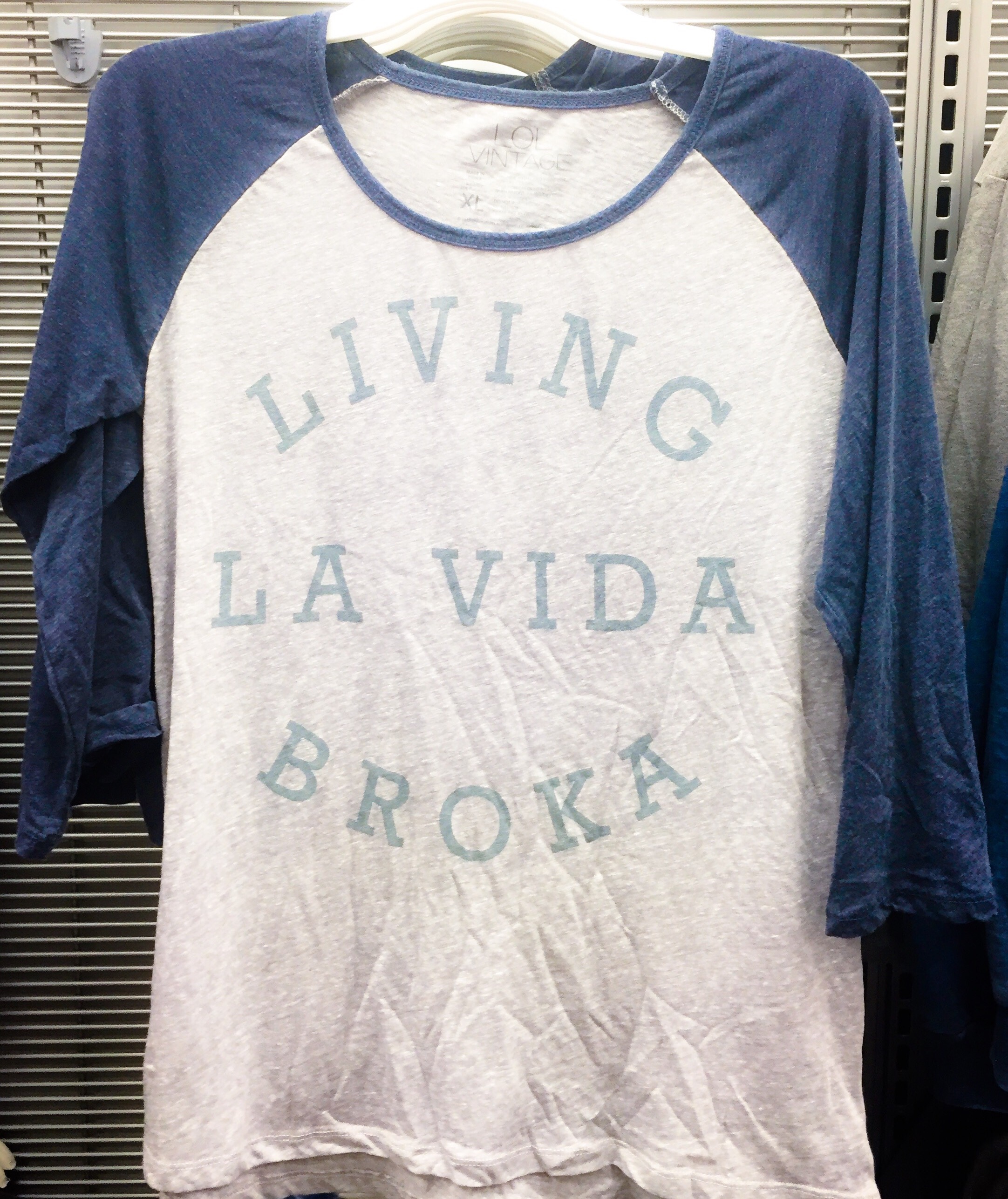

Practice “The Art of Saying NOPE” and you won’t have to wear THIS SHIRT instead:

Catch my drift?

~The Financial Hack ©2015

On a previous posting (September 15th) I mentioned a faster way to save your money was to save your singles (as in dollar bills.) As of yesterday’s count, I have saved $30. That’s an average of $10 in singles saved per week. If I continue to save at this rate, in one year, I will have $520. That money can be used to take a mini-vacation, invest, buy Christmas/birthday gifts, add it to my emergency fund or just simply save it. The options of what to do with the money are endless.

The way to accomplish “saving your singles” is to use the cash method. Withdraw your budgeted allowance at the beginning of each week… AND STICK TO SPENDING ONLY WHAT YOU’VE WITHDRAWN. Today, it is so easy to whip out and swipe our debit cards. My bank has the “Keep the Change” program, where the remaining change from a debit card transaction rounded up to the nearest dollar, is deposited (usually into a savings account) that’s tied to your checking account. I’m sure your bank has something similar. “Keep the Change” can be beneficial because it is often used as overdraft protection. The problem is, some banks charge a fee each time overdraft protection is applied. I try to keep a “cushion amount” of $200-$300 in my checking account to avoid these fees. The “Keep the Change” program works for some people, but how many people do you know actually allow the money from the program to accumulate over time, then withdraw it? I don’t know any. For me, the temptation to spend it is too great. Technically speaking, the only reason I keep the Keep The Change/overdraft protection savings account is to avoid paying the monthly fee for my checking account. I prefer the “Keep the Singles” method better. Truth be told, there’s something about the “tangible.” I can see the dollar bills, I can hold and count the dollar bills, and most importantly, I can sock the dollar bills away in my piggy bank… Then hide the piggy bank. Out of sight, out of mind right? Problem solved. Money Saved.

Let me know if you incorporate the “Save Your Singles” method or a similar method of saving money by commenting below. I’d love to hear from you.

~The Financial Hack ©2015

YOU CAN ORDER A “SHORT” SIZE OF YOUR FAVORITE COFFEE (OR DRINK) AT STARBUCKS?

The 8oz “short” size as compared to the 12oz “tall” size is Starbucks’ best kept secret. You’ll never see it on the menu (and probably never will) so be sure to ask for it specifically when ordering. The “short” is a STEP DOWN from the 12oz “tall” which most think is the chain’s smallest size. Not true. “Java Junkies” like myself already knew about the “short,” but usually go for the Venti or even the Trenta . For those who may be “trimming the fat” from their budgets and not yet ready to eighty-six the gourmet coffee experience all together, ordering the “short” size satisfies the gourmet coffee experience without blowing the budget. For a few extra coins, go ahead and ask for an extra shot… Of expresso that is. ENJOY!

~The Financial Hack ©2015

TIP TUESDAY: If you’re leery about “playing the stock market” and may be looking for a “safer” way to grow your money, consider purchasing a Certificate of Deposit (or CD for short.) CD’s are issued by banks, credit unions etc. and have the advantage of offering more competitive interest rates (APY) than traditional savings accounts. Check your banking institution for minimum amounts to purchase CDs as they can vary with each institution.

Some people may think you need large sums of money to purchase CDs. FALSE. $500 can easily get you started. REMEMBER, build your emergency fund of $1000 FIRST, then save an additional $500 and purchase a CD to start. Again CDs are a great way to save money because they yield higher rates. Wouldn’t you rather your money earn in upwards of 4% or better as opposed to <1% on a traditional savings account? I would. NOTE: The longer the duration of your CD, the higher the interest rate. For example, a 30 day CD may garner an APY of 1.75% whereas a 60 month CD may garner a higher APY of 5-6%. Keep in mind the percentages given are approximations ONLY. Unlike a traditional savings account, there is a penalty for partial/early withdrawals which will hopefully keep temptation at bay. Once the CD has reached its maturity, you’ll have the option to cash out, roll it over for the same duration of time or change the duration of your CD based on current interest/market rates. If you do nothing, the CD will automatically roll over for the same duration of time at the current market rate of interest.

Now, I am by no means advising anyone to take their savings and put it all into CDs. A Financial Advisor wouldn’t advise that. As a matter of fact, they would advise against it. NEVER put all your eggs into one basket. A well balanced financial portfolio is certain to yield pretty “decent” returns.

What has been your experience with CDs? Please let me know below. If purchasing CDs sounds like something that may be of interest to you by all means, visit your banking institution for more information. GOOD LUCK!!!

~The Financial Hack ©2015

A couple of months ago, I mentioned how I save all my coins and cash them in yearly. This year, I deposited approximately $300+ in coins into a separate savings account. But why should I stop there? Truth is, I don’t have to. In addition to saving my coins, here’s yet another easy way to save….

SAVE THOSE DOLLAR BILLS!!!

If I save my coins, why not save my dollar bills too? Starting today, I’m going to see how many singles I can save by September 15, 2016. Who dares to accept this challenge along with me? Are you ready? Synchronize your watches in 5, 4, 3, 2, 1…. GO!!!

Cha-Ching…. Now watch those dollars add up.

~The Financial Hack ©2015